Early in June the country was rocked by the allegations of financial misreporting on Rajesh Exports Limited (REL), Bangalore based company in gold business headed by Rajesh Mehta, involving massive revenue of ₹15.15 lakh crore ($158 billion). In its interim order, the Security and Exchange Board of India alleged that REL failed to make mandatory disclosure of revenues earned from its international subsidiaries. As the SEBI order notes, ‘more than 97% of REL’s reported consolidated revenue during FY 2020 – 21 to FY 2024 – 25 was attributed to its subsidiaries and step-down subsidiaries.’ For comparison of the consolidated revenue, consider that Adani Enterprises, one of India’s largest conglomerate businesses, reported a revenue of ₹4.3 lakh crore over FY 21 to FY 25; a fourth of that reported by REL.

The SEBI order further alleges, “however, despite repeated summons …..REL failed to furnish party wise breakups, sales registers, purchase registers, invoices, purchase orders or any other supporting documentary evidence.”

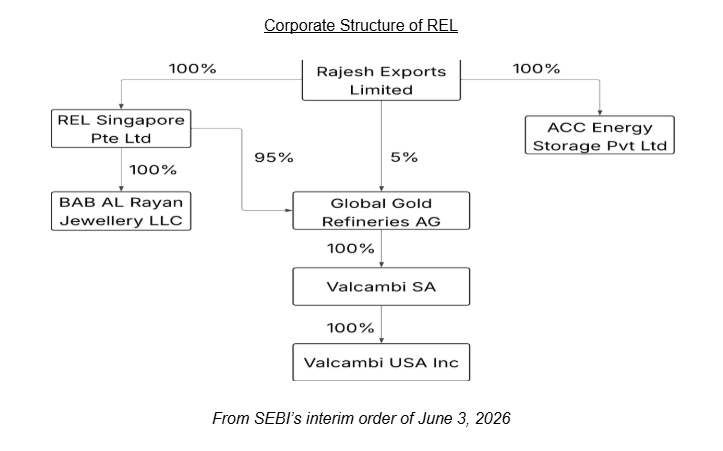

SEBI’s order charges REL with violations of the following rules. Section 136(1) of the Companies Act, 2013, which mandates companies with subsidiaries to place separate audited financial statements of each such subsidiary on their website. Something which the REL did not do invoking privacy laws of Switzerland where its subsidiaries Valcambi SA and Global Gold Reserve AG were based. Furthermore, SEBI alleges non-compliance with LODR (Listing Obligations and Disclosure Requirements ) Regulations which enjoin upon listed entities to publish the separate audited financial statements of every subsidiary on its website at least 21 days prior to the Annual General Meeting. For allegedly misrepresenting its financial indicators before investors and shareholders, SEBI charges REL with violation of the PFUTP (Prohibition of Fraudulent and Unfair Trade Practices) Regulations.

The SEBI order has been followed by Enforcement Directorate raids on the offices of REL.

And yet, the questions raised by the REL episode go far beyond the violations being investigated by regulators and agencies. They cast a dark shadow on India’s financial regulation and its ability to safeguard public interest and money.

It took a complaint from a shareholder two years back to get to this point. Even though red flags had been raised about REL’s financials for at least a decade. In 2014 Moneylife had highlighted how the reported figures by the gold trader did not add up. This begs the question: what was the securities watchdog, SEBI, doing all this while? Who monitors mandatory public disclosures being made by listed entities? Did the unusually high revenue figures not ring any alarm bells? Perhaps, not loud enough for the slumbering watchdog!

Similarly this raises questions on the public institutional investors such as Life Insurance Corporation, which continues to hold more than 10% stake in REL. What due diligence did they do before sanctioning the investment which was made over a decade bankrolled on public savings?

The non-chalance of public regulators and financial institutions becomes glaring against the caution exercised by private investors. Domestic mutual funds, reportedly, completely avoided Rajesh Exports because of the company’s fundamentally questionable financial metrics, notably its massive turnover combined with extraordinarily thin profit margins. Fund managers cited a lack of confidence in the reported revenue numbers, red flags they discovered during their due diligence, and concerns over cash flow. The same information was at the disposal of SEBI and LIC.

The REL episode is unfortunately yet another instance that serves to dent public trust in public institutions.

This article was originally published in Bank Beats, a fortnightly magazine by AIBOC, and you can read it here