Urgewald, a German environment and human rights NGO, which claims to be working for establishing strong environmental and social standards for the international finance industry, has called India “the number one hotspot of the coal mining boom” in the world. It states this in a report “The 2023 Global Coal Exit List (GCEL): Failing the Phase-Out”, prepared by Urgewald and more than 40 NGO partners, seeking to offer in-depth information on over 1,433 companies operating worldwide along the thermal coal value chain.

Urgewald, a German environment and human rights NGO, which claims to be working for establishing strong environmental and social standards for the international finance industry, has called India “the number one hotspot of the coal mining boom” in the world. It states this in a report “The 2023 Global Coal Exit List (GCEL): Failing the Phase-Out”, prepared by Urgewald and more than 40 NGO partners, seeking to offer in-depth information on over 1,433 companies operating worldwide along the thermal coal value chain.

Stating that India’s coal production “already reached a historic high of 893 million tons last year”, the report, released a few weeks after the UN’s Climate Ambition Summit in New York, quotes the goal set by India’s Ministry of Coal and Mines, according to which, the country’s annual coal production would rise to 1.5 billion tons by 2030.

“To fulfill this plan, the government has auctioned off 92 new coal mining concessions since 2020; hundreds more are in the pipeline”, says Urgewald in the report, which approvingly quotes Joe Athialy, director of the Centre for Financial Accountability, Delhi, as saying, “What is being auctioned off here are the traditional homelands of hundreds of thousands of India’s tribal people and forest areas that are incredibly rich in biodiversity and play a key role in maintaining water cycles. It’s absurd to pretend this immense destruction is in the national interest.”

Stating that of the top three coal mining developers, two are from India, the report says, “The world’s top three coal mine developers are Coal India with projects totaling 591 million tons of new coal production per year, China Energy Investment with 169 million tons and the Adani Group with 94 million tons.”

It continues, “While the first two companies are state-owned, the Adani Group belongs to the billionaire Gautam Adani whose business has profited time and again from his close ties to the Modi government. Today, Adani is the world’s largest private coal mine developer.”

The report adds, “The conglomerate owns coal mines in three countries, is a major trader and transporter of coal, operates a 16 GW coal plant fleet (with another 10 GW in the pipeline), and plans to build a huge US$ 4 billion coal-to- plastics facility in India. While one of the Adani Group’s 9 listed subsidiaries – Adani Green Energy – develops solar projects, the Group’s renewable investments are dwarfed by its enormous coal portfolio.”

Claiming that there is “a pervasive pattern of intercompany lending, including transactions between Adani Green Energy and Group entities involved in coal expansion”, about which controversial short-seller Hindenburg Research’s 106-page report and subsequent investigations state, the report says, “Filings by the State Bank of India have shown that shares from Adani Green Energy and other Group subsidiaries were used as collateral in a credit facility for Adani’s enormous Carmichael coal mine in Australia.”

“Adani is a stark example of why responsible investors need to divest all subsidiaries of coal developers. It’s an illusion to believe that investments in the green arm of a company aren’t cross-subsidizing its other activities,” comments Urgewald director Schuecking.

Profiting time and again from close ties with the Modi government, today, Adani is the world’s largest private coal mine developer

The report regrets, with over 7.2 billion tons, “the world’s thermal coal production reached an alltime high in 2022” with “new coal mines still on the horizon in 31 countries.” It adds, “All in all, companies on the GCEL are planning to develop new thermal coal mining projects with a total capacity of 2.5 billion tons per year, an amount equal to over 35% of the world’s current production” — with India all set to experience “coal mining boom”, as its coal production having reached “a historic high of 893 million tons last year.”

While releasing the the GCEL list, the report quotes Heffa Schuecking, director of Urgewald, says, “The overall picture that our data delivers is bleak. Out of the 1,433 companies on the GCEL, only 71 companies have announced coal exit dates. Meanwhile, 577 companies are still developing new coal assets.”

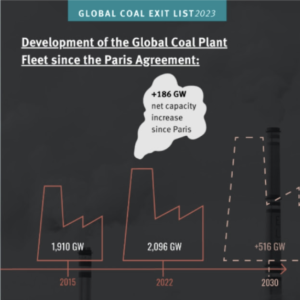

According to the report, “Despite coal plant closures in some parts of the world, the global coal plant fleet has seen a net growth of 186 GW since the Paris Agreement was signed. To put this into perspective: 186 GW are more than the operating coal plant fleets of Germany, Japan, South Korea and Indonesia combined.”

It continues, “According to the 2023 GCEL, companies are still planning to develop an additional 516 GW of new coal-fired capacity. If built, these projects would increase the world’s current installed coal-fired capacity by 25%.”

According o the report, “Two-thirds of this new capacity is planned in China, which has been ramping up its coal power plans since 2022, when drought diminished the country’s hydropower output and record-breaking heat waves caused electricity demand to skyrocket.”

It adds, “Out of the 39 countries where new coal power plants are still in the pipeline, the largest capacity additions are planned in India (72 GW), Indonesia (21 GW), Vietnam (14 GW), Russia (12 GW) and Bangladesh (10 GW).”

This article was originally published in Counterview and can be read here.

Centre for Financial Accountability is now on Telegram. Click here to join our Telegram channel and stay tuned to the latest updates and insights on the economy and finance.