Anirban Bhattacharya & Pranay Raj

A Reserve Bank of India statement on June 8 has set off a raging debate. The bank has allowed for write-offs and compromise settlements for even frauds and wilful defaulters frauds “without prejudice to the criminal proceedings underway against such debtors”.

A Reserve Bank of India statement on June 8 has set off a raging debate. The bank has allowed for write-offs and compromise settlements for even frauds and wilful defaulters frauds “without prejudice to the criminal proceedings underway against such debtors”.

Among those who have been extremely critical of the decision are the bank unions. “We have always advocated for strict measures to address the issue of willful defaulters,” the unions said in a statement. “We firmly believe that allowing compromise settlement for accounts classified as fraud or wilful defaulters is an affront to the principles of justice and accountability.”

Wilful defaulters are those who refuse to repay loans despite having capacity to do so.

The compromise settlement mentioned in the Reserve Bank statement means that the outstanding balances of these wilful defaulters may be settled by mutual concession, with dues not being recovered completely. Far from strengthening the means to recover loans from wilful defaulters, the statement speaks of resettlement of the outstanding amount by means of “technical write-offs”.

This has been one of the key ways through which the non-performing assets of public and private sector banks have been shown to be declining in the last few years. It has emerged like a magic wand that makes the bad debt disappear from the balance sheets.

The Reserve Bank, in a clarificatory Frequently Asked Questions note, has claimed that the permission for banks to engage in compromise settlement with wilful defaulters is not new. It also says that such compromises would be effect only at the “discretion” of lenders and on their “commercial judgment”.

It is precisely this “discretion” that seems to make things murky by giving defaulters an easy way out. But neither the Reserve Bank nor the government seem to be in the mood to address the rising trend of defaulters, outstanding debt and write-offs.

Write offs, frauds in recent years

Broken promises are as old as promises. But at least there is some accountability in play when someone accuses a government of reneging on its promises. In fact, that forms the essence of democracy. It does not portend well for the health of a democracy when the rulers are not even questioned frequently about their own promises.

In 2018, for instance, Prime Minister Narendra Modi boasted that his National Democratic Alliance had not granted even a single loan to parties who later defaulted on repayments. Taking a jibe at the Congress, he said, “Every penny of loans given at the behest of ‘naamdaars’ [dynasts] will be recovered.”

He was referring here to the non-performing assets crisis, a product of the Congress-led regime allowing risky loans in 2006-’08 when it was dizzy in its bubble of high growth. When these rich borrowers started defaulting, pressure was mounted on the banks to give them more time or to restructure the loans, Modi claimed.

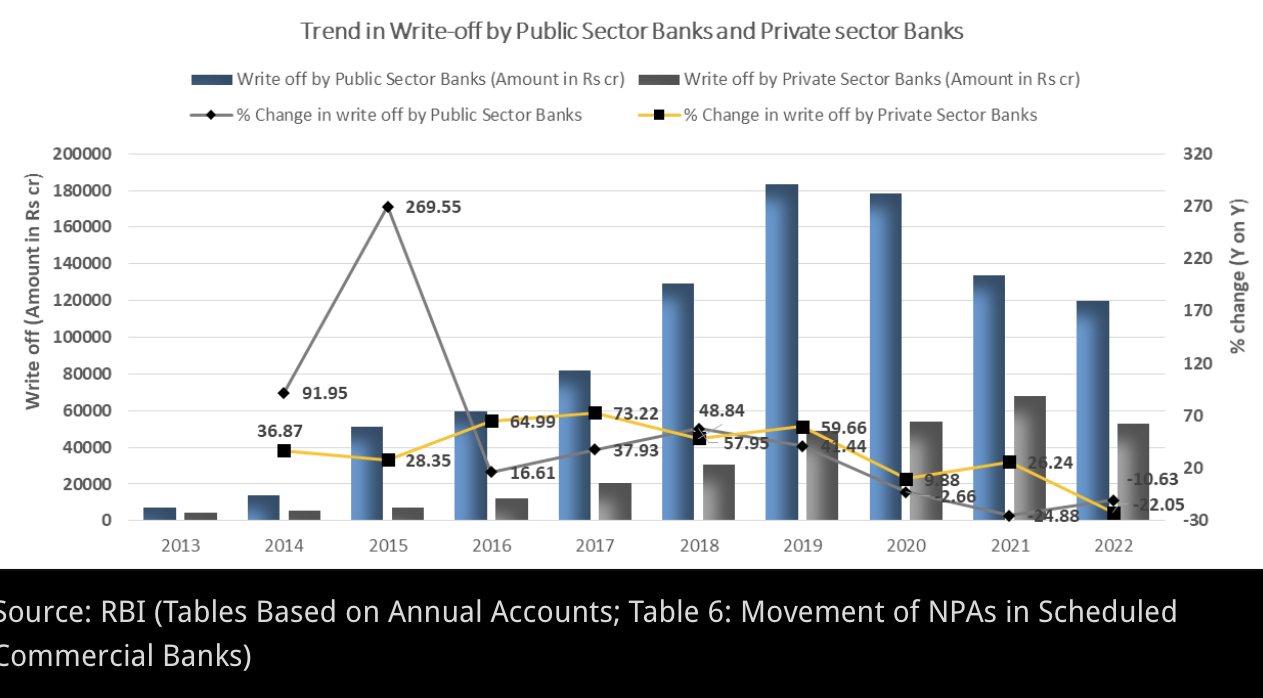

It is followed by Punjab National Bank at Rs 92,511 crore, the Bank of Baroda at Rs 75,429 crore and the Bank of India at Rs 53,961 crore.

For private sector banks, total write-offs increased from Rs 4,115.02 crore in 2013 to Rs 53,087.03 crore in March 2022. ICICI, Axis, and HDFC were the top three private-sector banks that wrote off the highest advances. Over the past ten years, ICICI Bank has written off loans amounting to Rs 71,198 crore, Axis Bank Rs 60,764 crore and HDFC Rs 43,633 crore.

Here is the graphic representation of the situation by both public sector banks and private sector banks over the past ten years with percentage change on yearly basis.

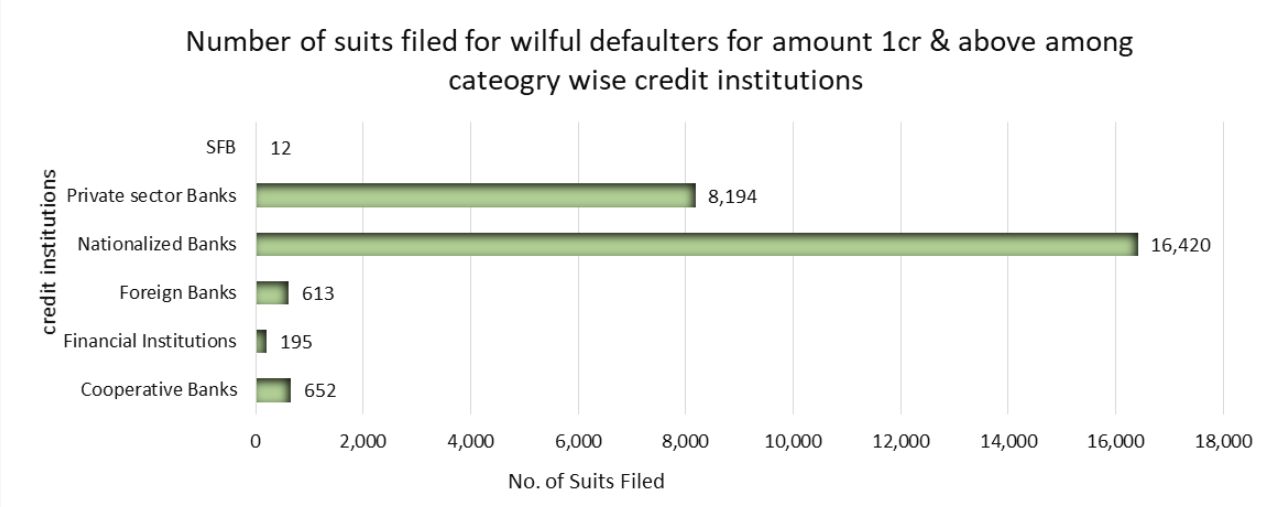

To obtain a fuller picture of the government’s record on defaulters, it is worth noting that the total number of suits filed by March 31 this year for parties who have defaulted on loans of Rs 1crore and above is 26,086. Their total outstandings are Rs 601,834 crore. Public sector banks filed 16,420 suits for loans amounting to Rs 410,758 crore.

Private banks filed 8,194 suits against parties who had defaulted on loans of Rs 1 crore and more. Together, these entities had failed to return Rs 168,031 crore.

The trend is apparent with relation to bank frauds. They rose nearly 17-fold from Rs 34,993 crore in the 2005-’14 period to Rs 5.89 lakh crore in the 2015-’23 period. That is nearly a 17-fold increase. The carefully curated image of a strong or decisive leader who would root out corruption proved only fictive.

‘Freebies’ for the rich

A lot has been made of welfare spending. Critics have described them as “freebies” or “revadi”, sesame candy, while state governments engaging in public spending haves been targeted as being “fiscal imprudent” or “irresponsible”. All this while enormous amounts of corporate debt have been wiped off the balance sheets of companies. Because the amounts are so gigantic, is often difficult for the common people to grasp the exact measure of such write-offs.

These examples may help put the figures in perspective.

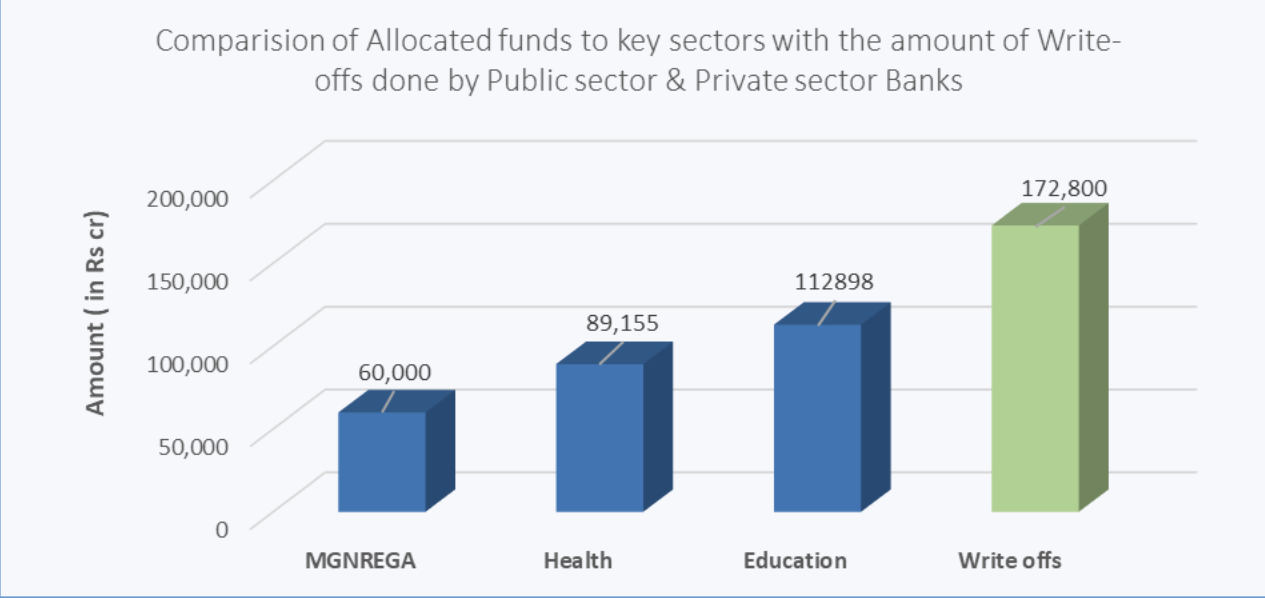

The tragic train accident at Balasore that left at least 292 people dead brought the question of spending on safety to the foreground. As per the Comptroller and Auditor General of India’s 23rd report of 2022, the funds spent upon the replacement of older tracks was not sufficient. The combined shortfall in the money needed for the renewal of tracks amounts to Rs 103,395 crore. By comparison, the write-offs that year by public sector banks alone amounted to Rs 133,945 crore.

The total write-offs by public sector banks and private sector banks in the 2021-’22 financial year stands at Rs 1,72,800 crore, which is much higher (see figure below) than the amount allocated to any of the three key social sectors in 2023-’24. Demands to even slightly increase the blue bars raise eyebrows, but with the recent changes we are paving the path to increase the write-offs.

If this amount of public money being written off does not receive airtime in our national media and if Indians do not end up demanding answers from our rulers about their promises, it will demonstrate the complete collapse of a system of public accountability that is a cornerstone of democracy.

This article was originally published in Scroll.in and can be read here.

Centre for Financial Accountability is now on Telegram. Click here to join our Telegram channel and stay tuned to the latest updates and insights on the economy and finance.