The Deposit Insurance and Credit Guarantee Corporation (DICGC) has implemented a risk-based premium system from April 1, 2026, replacing the flat rate structure and linking premiums to banks’ risk profiles.

The Deposit Insurance and Credit Guarantee Corporation (DICGC or “Corporation”) has implemented a Risk-Based Premium (RBP) framework for deposit insurance with effect from April 1, 2026. This marks an important shift in how banks pay for deposit insurance.

For years, all banks paid the same premium rate to the DICGC. Under the new framework, the premium a bank pays will depend on how risky the bank is assessed to be. Although the move had been under consideration for several years, the Reserve Bank of India (RBI) first formally announced it in October 2025, replacing the flat premium system with a framework that differentiates banks based on their risk profile. Following the approval of RBI’s Central Board in December 2025, the DICGC, a wholly owned subsidiary of the RBI, issued the detailed framework in February 2026 which came into effect from April 1.

Why Do We Need Deposit Insurance?

Banks enter into something known as maturity transformation. This means they accept deposits from the public that can be withdrawn on demand or at short notice. These deposits are then used to make long-term loans such as housing loans, business loans, or infrastructure financing. Banks earn income by charging higher interest on loans than what they pay on deposits, with the difference (also called net interest income) traditionally being one of the primary sources of income for banks. This creates an inherent fragility in banking. If depositors begin to worry that a bank might fail (even if the concern is based only on rumours) they may rush to withdraw their deposits before others do. If enough depositors do this simultaneously, the bank may run out of liquid funds and fail, even if it was otherwise fundamentally solvent.

Deposit insurance was introduced to reduce this risk by guaranteeing deposits up to a certain limit if a bank fails. This helps prevent panic withdrawals and “bank runs”. In return for providing this guarantee, banks pay a premium to the deposit insurance authority. Deposit insurance therefore serves several purposes. It protects small depositors, prevents panic withdrawals, and contributes to financial stability by reducing systemic risk.

This modern form of deposit insurance emerged globally after the Great Depression in the United States when widespread bank failures led to the creation of the Federal Deposit Insurance Corporation. In India it was introduced in 1961 following a series of bank failures.

How Deposit Insurance Works in India

In India, the system of deposit insurance is administered by the DICGC. Banks contribute regularly (a premium) to an insurance fund maintained by the DICGC. If a bank fails, the DICGC uses this fund to compensate depositors up to the insured limit (the insurance cover).

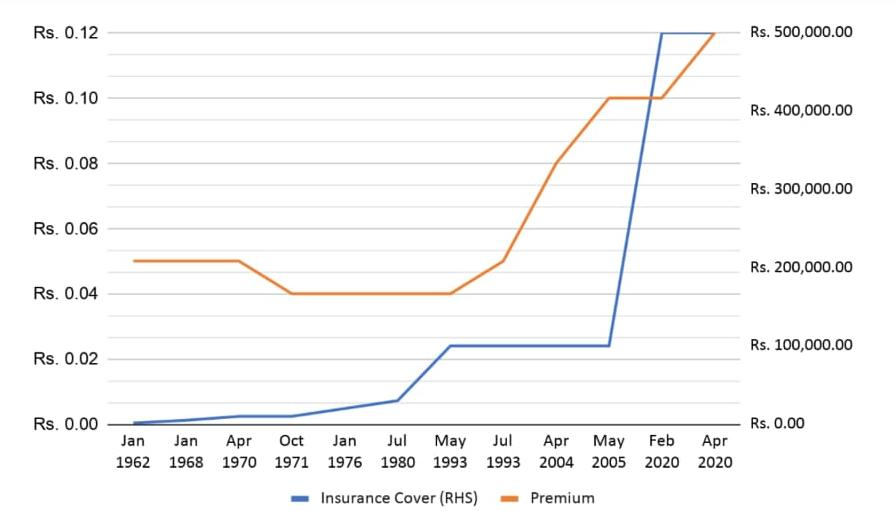

Under the flat premium system previously in place, every insured bank paid the same premium of 12 paise for every Rs. 100 of assessable deposits per year to the DICGC. The deposit insurance coverage limit, last revised in February 2020, is Rs. 5,00,000 per depositor per bank. Both the insurance coverage limit and the premium rate have been revised several times over the years.

Image: Historical Progression of Deposit Insurance Coverage (Source: DICGC)

Image: Historical Progression of Deposit Insurance Coverage (Source: DICGC)

While the flat premium system is simple to administer, it is often argued that it has one important drawback: it treats all banks the same regardless of how prudently they manage risks.

The case against a Flat Premium System

The RBI argues that the move towards a risk-based premium framework is intended to incentivise sound risk management by banks and reduce premiums paid by better rated institutions.

Unlike in health insurance where lower-risk entities typically pay lower premiums, under the earlier flat premium system, all banks paid the same rate regardless of risk. This creates what is described in economic literature as a moral hazard. Moral hazard arises when a person or institution is protected from the consequences of their actions. Because the negative consequences are partly borne by someone else, the incentive to behave cautiously becomes weaker. In the context of deposit insurance, a similar concern is argued to arise. The data on claims settled by DICGC is often used to further this argument. During 2024-25, the Corporation received total premium income of Rs. 26,764 crore. Commercial banks (including Regional Rural Banks and Local Area Banks) contributed Rs. 25,352 crore (or about 94.7%). Cooperative banks contributed the remaining Rs. 1,412 crore (or about 5.3%). In contrast, during the same year, the Corporation settled claims worth Rs. 476 crore, all of which were related to cooperative banks. Since the inception of deposit insurance, the Corporation has paid Rs. 16,940 crore in claims. Of this amount, only Rs. 295.85 crore (1.75%) relates to 27 commercial banks, while Rs. 16,844 crore (more than 99%) has been paid in relation to cooperative banks. This mismatch between contributions and payouts is often cited in support of linking premiums to the risk profile of banks.

The new Risk-Based Premium Framework

With effect from April 1, 2026, the DICGC has introduced a Risk-Based Premium (RBP) framework under Section 15(1) of the DICGC Act, 1961, which allows differential premium rates for different categories of insured banks.

Two risk assessment models are used – Tier 1 and Tier 2. The Tier 1 model will apply to Scheduled Commercial Banks (excluding Regional Rural Banks). It will incorporate objective financial parameters to assess risk. The Tier 2 model will apply to Regional Rural Banks and cooperative banks. This model will rely on corporate governance parameters in addition to financial parameters. Banks will then be classified into four categories (A to D) based on their assessed risk.

| Rating Category | A | B | C | D |

| Current Premium card rate | 12 | 12 | 12 | 12 |

| New Premium card rate | 8 | 10 | 11 | 12 |

| Discount over card rate | 33.33% | 16.67% | 8.33% | 0% |

Rating Categorisation and Premium Rates (Source: Risk-Based Premium Framework)

Local Area Banks and Payments Banks, due to insufficient data, and all Urban Co-operative Banks under RBI’s regulatory oversight will continue to pay the current rate of 12 paise per Rs. 100 of deposits.

The framework also introduces a “vintage incentive”, offering banks an additional discount of 1% for each completed year of stable operations capped at 25%. This benefit will reset if the bank undergoes significant stress or restructuring.

The effective premium rate, then, as per the framework will be calculated as:

To understand how this works, consider the two extreme cases under the framework:

|

Lowest-risk bank (Category A + 25 years vintage) |

Highest-risk bank (Category D + no vintage) |

|

| Card Rate | 12 paise | 12 paise |

| Risk Model Incentive | 33% | 0% |

| Vintage Incentive | 25% | 0% |

| Effective Rate |

|

|

In effect, a financially strong bank could pay half the premium of a high-risk bank. The new framework therefore claims to introduce a clear financial incentive for banks to maintain stronger balance sheets and better risk management practices.

The framework also allows the DICGC to override ratings if significant adverse developments emerge after the initial assessment. Banks are also required to keep their ratings confidential to ensure that the disclosure of a bank’s risk rating does not itself trigger panic withdrawals by depositors. To support this objective, disclosure requirements have also been modified. Earlier, banks were required to disclose the amount of deposit insurance premium paid to the DICGC. Under the new framework, banks are now required to just state in their annual reports that “deposit insurance premium as applicable was paid to DICGC within the prescribed time.” This change is intended to prevent depositors from inferring a bank’s risk category from the premium amount paid.

While this explains the logic behind the framework, it raises several concerns.

Beyond Premium Pricing

Banks that are already financially weaker are less likely to qualify for premium discounts and may therefore face higher insurance costs relative to stronger institutions. This could make it more difficult for them to compete for deposits, particularly if depositors begin to perceive them as riskier. This issue is especially relevant for cooperative banks and Regional Rural Banks, which often serve smaller depositors and underserved regions. If these institutions face relatively higher costs, it could affect their ability to continue serving these segments effectively. The framework may also be pro-cyclical: banks under stress could face higher premiums precisely when they are least able to bear them.

More broadly, the framework relies on the ability to accurately measure and price risk. In practice, risk assessment is complex and often based on past performance and supervisory indicators. Risk assessment is inherently backward-looking, meaning pricing may lag underlying deterioration. At the same time, this approach may not fully capture the role some banks play in serving smaller depositors and underserved regions. If pricing is based mainly on risk indicators, it raises the question of whether and how these developmental functions should be factored into the pricing of premiums.

Beyond these design-related concerns, one important concern relates to the treatment of the Public Sector Banks (PSBs). As noted by Devidas Tuljapurkar, PSBs operate with an implicit sovereign backing because of their government ownership. In such a context, the rationale for charging deposit insurance premiums on PSBs (whether flat or risk-based) becomes less clear, as depositors already perceive these banks as relatively safe. A related argument extends to private sector banks. Even without explicit sovereign backing, past experiences (such as in the case of Yes Bank) reflect “too big to fail” dynamics. As Tuljapurkar argues, this raises questions about the practical relevance of deposit insurance for large private banks, where systemic considerations often prompt public intervention.

Another issue is how premiums are calculated. Banks currently pay deposit insurance premiums on their entire assessable deposit base, even though the insurance covers only Rs. 5,00,000 per depositor. This means the banks are also paying for deposits that are not actually insured. Whether premiums should instead be more closely aligned with insured deposits is an important policy question that remains unaddressed.

The move to risk-based pricing aligns India’s deposit insurance system with global practices. However, it also raises fundamental questions about how deposit insurance is designed and what it is expected to achieve. Balancing financial stability, depositor protection, and the broader public role of banking will remain central as the framework is implemented and undergoes periodic review (at least once every three years as mentioned in the framework) in the years ahead.

Rohit Patwardhan is a researcher at the Centre for Financial Accountability, working on energy policy, public finance, and their intersection.

This article was originally published in Kanal you can read it here.