Women bear the burden of a lending system that profits from chronic financial distress as they borrow to pay for food, healthcare and survival.

Forty-five-year-old Shabreen (name changed) lives with her two sons and three daughters in a hovel near Faridabad, Haryana. At one point, she ran this household of six while working as a nurse. These days, her oldest son is the main earner, while she and her daughters do odd jobs apart from household chores. The slum that they reside in is in an area that floods for about a month every five years; as it did in September 2025, when the National Capital Region (NCR) experienced heavy unseasonal rains.

Most houses here have tiny rooms and are generally a couple of stories tall, accessible by narrow, muddy paths. The homes are surrounded by small hills of garbage. After every flood, parts of the buildings are destroyed, incurring significant renovation costs, especially on the electrical and plumbing lines.

Evidence of the landfill near the slum. The area was water-logged on January 31, 2026, after 25.4mm of rainfall over the month. Photo: Samali Banerjee

The first time Shabreen took a loan was to build her house. She explained how they bought the small piece of land in the colony by taking out a loan from their neighbouring money-lenders (whom she refers to as ‘the Gujjars’), just before her oldest daughter’s marriage.

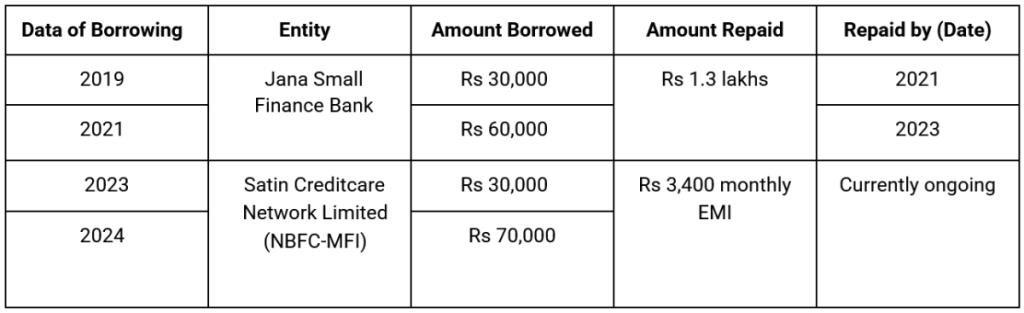

They used the loan to build part of the house, after which she borrowed Rs 30,000 in 2019 from Jana Bank, a Small Finance Bank (SFB). In 2021, she borrowed another Rs 60,000, repaying it entirely by 2023 – a total of Rs 1.3 lakh on a cumulative principal of Rs 90,000. Later that year, she borrowed Rs 30,000 from Satin Creditcare Network Limited, a microfinance institution (MFI), followed by an additional Rs 70,000, towards which she continues to pay a monthly EMI of Rs 3,400.

Illustration of the loans taken out by Shabreen. (Samali Banerjee)

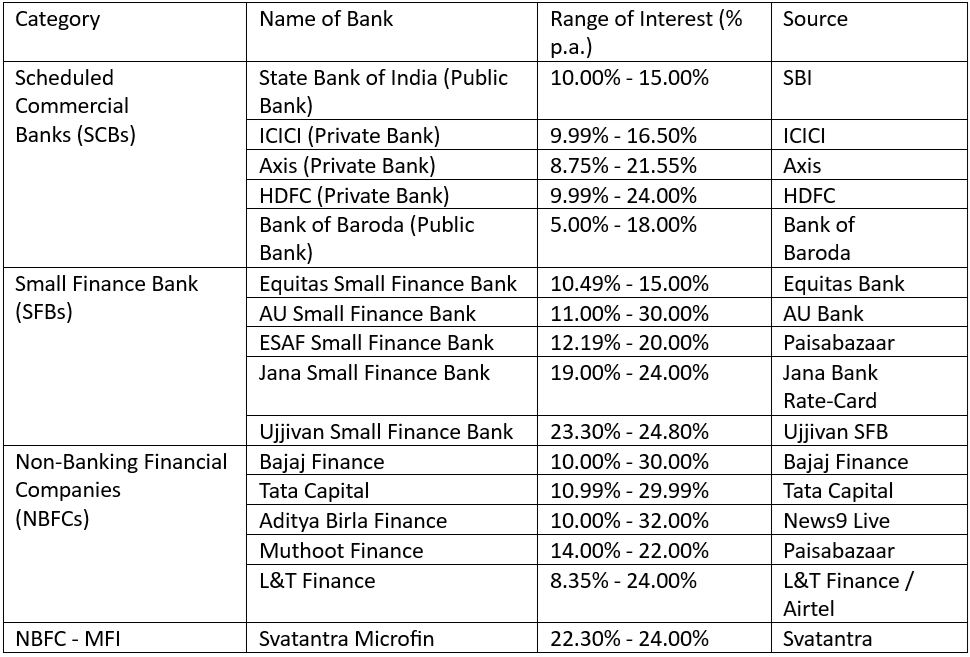

What are Small Finance Banks?

SFBs were launched in 2014 with one key distinction from Non-Banking Finance Companies (NBFC): the ability to hold demand deposits, which customers can withdraw at any time.

In practice, their lending operations are nearly identical to those of NBFCs or MFIs – supplying credit to small businesses, marginal farmers and unorganised sector entities through what they call high-tech, low-cost operations. Low cost here refers to the lender, though, not the borrowers.

Many SFBs, including Jana Bank, charge steep interest rates, which are justified as necessary incentives to lend these collateral-free amounts to “high-risk borrowers”.

The top five Scheduled Commercial Banks, Small Finance Banks and Non-Banking Financial Companies, along with the interest rates they charge per annum on personal loans. (Samali Banerjee, from public documents)

According to a report by the Microfinance Institutions Network, almost 99% of clients – the borrowers – are women. This is done under the guise of women’s ’empowerment’ and ‘increasing access to credit’. Yet it is consistently evident across conversations with the women borrowers that the men of these households are the decision-makers regarding how the borrowed money would be spent.

In reality, women also have far fewer resources to ‘abscond’ from their localities, unlike their male counterparts, and are also stereotypically considered more responsible, honest and ‘virtuous’.

According to the Time-use Survey, 2024, females spent 16.4% of their time on unpaid domestic work, compared to 1.7% for males. This means that recovery agents are far more likely to find them at home when they make their collection rounds. Women are also more visible to their neighbours, who notice these visits of recovery agents, making them more vulnerable to social ostracism.

This has been widely noted in the literature as the “economy of shame” that uses social norms to control the flow of money. This results in debt traps for people who are borrowing to survive, particularly women.

Muthoot Finance Limited, Annual Report 2024-25, page 4 of 422.

While sipping tea, Shabreen revealed that her husband had taken out a loan of Rs 3.5 lakh from ‘the Gujjars’ before he abruptly left home, leaving her to manage the debt repayment. She continued: “He tends to do this – take loans or items from the house and run off. He stays home for six months or so, then randomly leaves for 2-3 years, before returning again after much pleading with us,” he says.

This has been happening for the past 10-12 years. Shabreen’s relatives had brought him back during the Covid-19 lockdown by threatening and persuading her and her children. “We were compelled to keep him at home,” she said. Shabreen became pregnant then, she says, and he “threw me off a moving bike by pushing me with his elbow”.

The autorickshaw behind them braked very hard, saving her from near death, but Shabreen suffered injuries everywhere. The unborn child was unharmed. “It happened at this crossing, by the police chowk,” she says.

Does she have any active loans? Shabreen has a Rs 10,000 MUDRA loan and another of Rs 25,000 drawn from Baroda Bank, for which she had paid Rs 1,500 the month she took it out. “We had some money troubles recently. None of us had a job and my son wasn’t well, so we couldn’t afford to buy food or medicine. That is when we took a loan of Rs 20,000 from a moneylender at an interest rate of 10% per month,” Shabreen says.

She took out a MUDRA loan to repay it, which cost the family “only Rs 800 per year”, making it a much cheaper alternative. “At that time, my youngest contracted typhoid, so we needed to hospitalise her for nearly fifteen days,” she says.

Although designed as collateral-free credit for income-generating activities, an increasing number of MUDRA loans are now being drawn for consumption-smoothing purposes.

Shabreen raises a few chicken and goats at home. When asked if that earns her enough for a living, she said that most of the goats die during the harsh winters. If the goats do survive, they are sold during Bakr Eid, but they fetch only Rs 10,000-15,000 per goat.

She has one goat left, but says it will not make her a profit this year. Her plan is to sell desi chicken eggs for Rs 20 or Rs 25, since they sell well during the winter, not as much in the summer.

Shabreen’s eldest son earns between Rs 10,000 and Rs 12,000 a month from working at a local store, and insists that his mother rest. As a result, nearly 40–50% of their household income goes towards debt servicing, with the automatic debits of Rs 3,400 at Satin Creditcare and Rs 1,500 at Baroda Bank, totalling nearly Rs 5,000 a month before they buy any food or medicine.

Professor Dipa Sinha, Associate Professor at Azim Premji University, says that indebtedness has increased even in rural areas, but that is not as widely covered as in urban areas. Most of the debt is EMI-based, she points out, taken from NBFCs for consumption purposes, such as for health issues or marriages. Since these loans are rarely taken for productive purposes or income-generating activities, it has been observed that one loan is taken to repay another.

Not just Shabreen

Thirty-six-year-old Pooja (name changed) says she had purchased a touchscreen phone for her daughter’s education, financed on EMIs, with Bajaj Finance Limited – a deposit-taking NBFC – as the third-party intermediary. On one occasion, her salary was delayed by two days, leaving insufficient funds for an automatic debit.

Bajaj Finance charged her a Rs 600 penalty. A seemingly paltry sum, but for someone earning between Rs 500 and Rs 800 per day, with several dependents, these penalties compound into everyday anxieties.

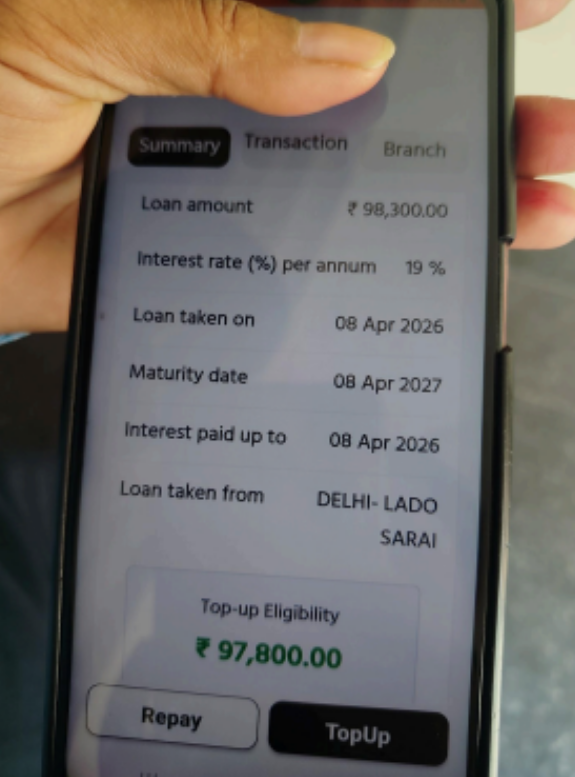

Forty-three-year-old Pramila (name changed), who works as a security guard, says she has had to borrow Rs 98,300 from Muthoot Finance, another deposit-taking NBFC, at an interest rate of 19% per annum, for what she said was a “deeply personal reason.” When she showed me the app, one feature stood out very clearly: a prominent button labelled “Top-Up”.

The language resembles that of a prepaid SIM card, and the messaging is vague, leaving ample room for misunderstanding. If an accidental click results, she would have just taken out her second loan even before she understood what was happening.

This NBFC was encouraging her to take this second loan – of a whopping Rs 97,800 – because she was meeting her repayment schedule on time, including the interest payments, which benefited the company and assured it of her ability to repay.

These nudges and patterns “in the algorithm” banking/NBFC apps using reveal the extractive logic built into the system.

Pramila’s phone screen containing the loan details, with very clickable nudges prompting further borrowing. Photo: Samali Banerjee

Drawn into taking loans at a time of severe distress, Pramila has kept the loan a secret from her family, and has refrained from discussing it even with her colleagues. She earns Rs 23,000 a month. Her sense of security now comes from her husband having recently secured a job in Oman as an HVAC (heating and air-conditioning) technician.

The family also carries education loans of over Rs 3 lakhs and additional loans taken to secure the husband’s visa and passage to Oman. One member migrating abroad as a labourer has become this family’s best hope.

The ‘pay for votes’ – or cash doles on offer for women – as electoral sops, as witnessed in Madhya Pradesh, Maharashtra, West Bengal and more recently in Bihar and Kerala – have their background in acute cash scarcity that women confront as they try to secure their own lives and that of their dependents. Some states have come up with programmes to relieve some of this distress, like Kerala’s Kudumbashree, a women-led cooperative network.

But in most other states, women confront only microfinance companies and their business logic, which leaves them deeply trapped in debt cycles that are often impossible to escape.

While nearly all the people I met in the peri-urban fringes of the NCR are close to repaying their series of loans, the strain on the system is palpable. In parallel, new firms offering loans have mushroomed as the valuation of the indirect credit sector continues to rise, while people are desperately borrowing for survival. The situation is alarmingly close to a crisis.

Dr R. Ramakumar, Professor at the Centre for Study of Developing Economies in the Tata Institute of Social Sciences, Mumbai, says, “Over the last two or three decades, we have seen the policy-inspired entry of private financial institutions into lending to the urban poor. This has been defended by its proponents using phrases like “profits at the bottom of the pyramid”.

But in reality, he explains, private financial institutions have meant the entrenchment of deeply exploitative financial agents in the urban credit market. The urban poor have been enticed into taking multiple loans on onerous terms, which, over time, have pushed them into deep debt traps.

These debt traps force them to take new loans, which are first used to repay the old loans. This becomes a vicious cycle that constantly erodes their capital and, increasingly, their ability to break even.

We have witnessed this before: the Andhra Pradesh microfinance crisis of 2010 began the same way. Loan repayments dropped to nearly zero, leading to severe liquidity crises for major MFIs. This represented the supply-side crisis.

On the demand side, the sudden halt in credit disrupted the financial safety net, limiting access to emergency funds for many rural households, and nearly 25,000 to 30,000 people lost their jobs. This period was also marked by coercive recovery practices and reports of borrower suicides that prompted district authorities to intervene.

In light of these experiences, it is time to better regulate the sector, particularly the interest rates that SFBs and NBFCs can charge. This is the obvious starting point, while the urgent question is whether we are willing to wait for another collapse before taking action.

Samali Banerjee is a Smitu Kothari Fellow (2025) established by the Centre for Financial Accountability, and a recent graduate in Economics from the South Asian University, New Delhi.

This article was originally published in The Wire and you can read it here.