Social protection and social security are crucial components of a country’s development agenda. Social security mechanisms not only reflect economic growth but also indicate the capacity of the state to deliver welfare to its poorest and most marginalised populations (Sülzer 2008). The International Labour Organisation (ILO) defines social security as ‘the set of policies and programmes designed to reduce and prevent poverty and vulnerability across the life cycle’. Its core components include child and family benefits, maternity protection, unemployment support, employment injury benefits, sickness benefits, health protection, old-age benefits, disability benefits and survivors’ benefits, financed through a combination of contributory schemes and tax-funded non-contributory programmes (International Labour Organisation 2021). Expanding this framework, Amartya Sen and Jean Drèze define social security as ‘the use of social means to prevent deprivation and vulnerability’, emphasising not only ‘protection’ but also the ‘promotion’ of wellbeing. In this view, social security is not merely the replacement of lost wages; it ensures that individuals can sustain basic capabilities and living standards even under adverse conditions (Drèze and Sen 1991).

In India, social security has developed in distinct phases shaped by the political economy of the time. In the early years after independence, protections were created primarily for industrial and formal-sector workers through legislation such as the Employees’ State Insurance Act, 1948 and the Employees’ Provident Fund Act, 1952. As a result, the system remained occupationally narrow, leaving most workers outside any form of income security, since the focus was on the organised sector rather than the workforce as a whole (Rajan 1999).

Following the green revolution, rural social protection expanded through the introduction of public works and wage employment schemes, marking a shift from industrial labour protections to rural social protection (Tillin 2025). The period also saw the emergence of state-level initiatives for the elderly, such as grants-in-aid1 to voluntary organisations for day-care centres and old-age homes, as well as modest non-contributory pensions for the ‘destitute aged’. However, these programmes remained limited in scale and uneven in their implementation (Rajan 1999).

In the 1990s, a more transformative concept of social security began to take shape, informed by a rights-based approach to welfare. During this period, the state expanded its role by translating commitments under the Directive Principles of State Policy into concrete entitlements.2 This marked a normative shift in social policy from discretionary relief to basic obligation of the state, articulated through the language of rights, citizenship and social justice (Tillin 2025). It was in this context that the National Social Assistance Programme (NSAP) was introduced in 1995, marking the first attempt to establish a national, non-contributory social assistance pension system for the country’s most socially and economically vulnerable populations.

While the late 1990s and early 2000s saw the strengthening of NSAP, subsequent decades have revealed structural gaps in India’s social security pension architecture. The system remains fragmented and is increasingly unable to respond to changing demographic and economic realities.

India, like other countries in Asia, is facing an unprecedented crisis of a rapidly ageing population (Irudaya, Rajagopalan and Kumar 2025). The number of older persons is projected to increase from 100 million in 2011 to 230 million by 2036. Many continue to work beyond the age of sixty, not by choice but due to unstable incomes, limited savings and the inability of households to absorb shocks. With more than 90 per cent of the workforce engaged in low-wage informal work without retirement savings or employer-backed protection, most older persons lack access to formal pensions and depend on social assistance, leaving them highly vulnerable to poverty (International Institute for Population Sciences and United Nations Population Fund 2023). The India Ageing Report of 2023 notes that 18.7 per cent of older persons have no income at all. Single women, widows, deserted women and those without family support, as well as persons with disabilities (PwD), face similar income insecurity and rely on social assistance for basic survival. These vulnerabilities are further compounded by intersecting inequalities of gender, caste and class.

Countries with comparable or lower gross domestic product (GDP) per capita, such as Nepal, Lesotho, Kenya and Bolivia, provide more expansive social protection than India. India’s Economic Survey 2025 notes that a wider pension system is needed, as pension assets account for just 17 per cent of GDP compared to 80 per cent in advanced economies (Ministry of Finance 2025). While pension schemes exist for formal sector workers, informal workers remain largely excluded and rely on social security and contributory pensions schemes such as the National Pension System (NPS) or the Atal Pension Yojana (APY) (Ministry of Labour and Employment 2026). Participation in these schemes remains low because many workers cannot afford regular contributions (Sharma and Pathak 2024).

Social security pensions are therefore a basic requirement of an inclusive social protection system. They recognise that individuals engaged in unpaid care work or low-paid informal labour, are entitled to income security in later life. A rights-based framework rests on the idea of ‘full citizenship’, understood as full inclusion – civic, political, social, economic and cultural – under which the state is obligated to guarantee a minimum level of dignity and protection (Jayal 2013).

13.1 National Social Assistance Programme

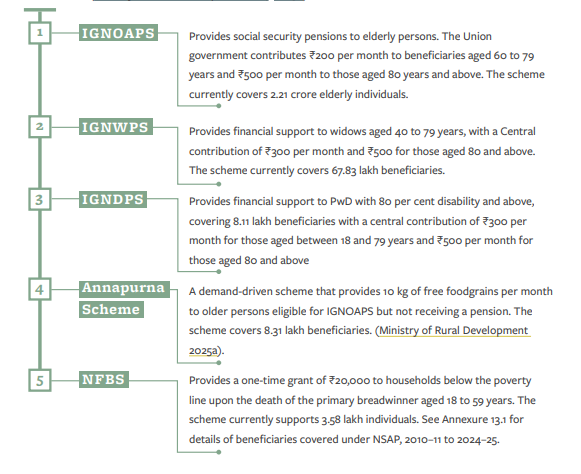

The National Social Assistance Programme (NSAP) was launched on 15 August 1995 with three components: the National Old Age Pension Scheme (NOAPS), the National Family Benefit Scheme (NFBS) and the National Maternity Benefit Scheme (NMBS). On 1 April 2000, the Annapurna Scheme was introduced to provide food security to senior citizens who were eligible but not covered under NOAPS. The NMBS was transferred from the Ministry of Rural Development (MoRD) to the Ministry of Health and Family Welfare on 1 April 2001. The Supreme Court in the ‘Right to Food case’ (PUCL v. Union of India & Ors., CWP No. 196/2001) recognised payments for the National Old Age Pensions as part of the entitlement framework for food security, directed that pensions be paid by the seventh day of each month, and that the scheme not be restricted or diluted without the permission of the Court.

The National Old Age Pension Scheme was renamed as Indira Gandhi National Old Age Pension Scheme (IGNOAPS) in 2007. In February 2009, two additional schemes – the Indira Gandhi National Widow Pension Scheme (IGNWPS) and the Indira Gandhi National Disability Pension Scheme (IGNDPS) were introduced.

Figure 13.1: Schemes under NSAP

The design and implementation of NSAP are outlined in guidelines issued by the MoRD, which define eligibility criteria, age thresholds, documentation requirements and payment norms. NSAP comprises five schemes (Ministry of Rural Development 2014; 2025b)

NSAP covers both rural and urban areas. Under this framework, the Central government provides a fixed amount of social assistance per beneficiary, based on state-wise beneficiary lists determined by the MoRD. States are expected to provide ‘top-up’/additional amounts from their own budgets, matching or exceeding the central assistance [Comptroller and Auditor General of India (CAG) 2023]. The central beneficiary cap is based on population data from the 2001 Census and poverty ratios estimated by the Planning Commission in 2004–05 (Directorate of Census Operations, Rajasthan 2001; Press Information Bureau 2007; CAG 2023). The guidelines also mandate monthly disbursement of pensions directly into beneficiaries’ bank or post office accounts under the direct benefit transfer (DBT) system.

13.2 Performance, analysis and implications

Despite the existence of a non-contributory social security programme, the implementation of NSAP has not kept pace with current socio-economic realities, often violating its own procedural guidelines. The programme’s design remains flawed, with low coverage and inadequate benefit levels and has seen little change over the past two decades. As a result, entitlements under NSAP remain limited and difficult to access.

13.2.1 Unrevised amounts

At the time of its launch, the central contribution under IGNOAPS was ₹75 per month, later raised to ₹200 in 2007. Since then, there has been no revision in central pension amounts. Under IGNWPS and IGNDPS, the initial central contribution was ₹200, later revised to ₹300 in 2012 (CAG 2023). Despite recommendations from various government and parliamentary standing committees,3 these amounts have not been revised for 18 and 13 years, respectively. The government reiterated in August 2025 that there are no plans to revise them (Ministry of Rural Development 2025b). These amounts, neither revised nor indexed to inflation, remain grossly inadequate to provide even a minimum level of protection. A comparison with countries having similar GDP per capita indicates that social security pension systems in these countries are typically broader in scope and provide higher benefit levels than India’s. Detailed cross-country comparisons are presented in Annexure 13.2.

13.2.2 Criteria and coverage

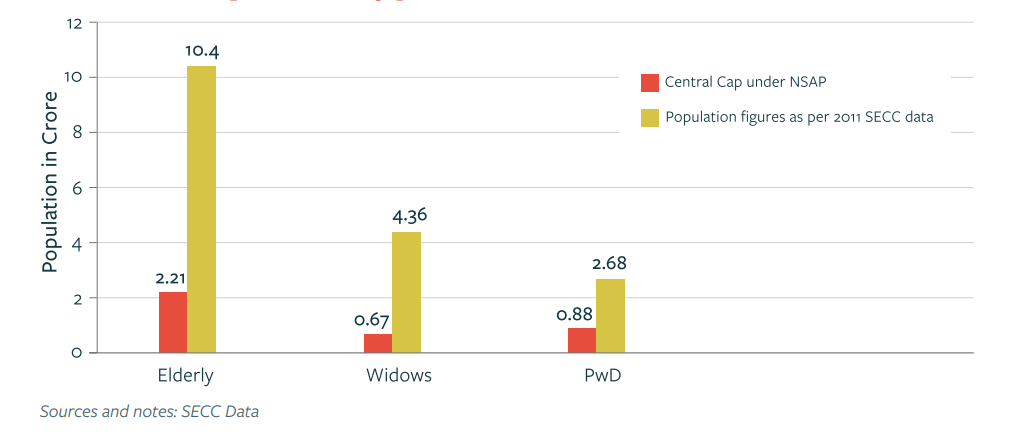

Unlike other welfare schemes that use the 2011 Socio-Economic and Caste Census (SECC) data to determine beneficiaries, NSAP caps the beneficiary base for its three pension schemes at 3.09 crore (Department of Economic Affairs 2025). See Annexure 13.1 for beneficiary coverage under each sub-scheme from 2011–12 to 2024–25 which has never exceeded 3.09 crore.

As the ceiling is neither defined by administrative capacity nor the actual number of eligible rights holders, eligibility as determined in the guidelines does not translate into an entitlement in practice. Section 3.1.3 of the guidelines also requires proactive identification of newly eligible beneficiaries, but this is not carried out on the ground, constituting a direct violation of the scheme’s own provisions. According to the India Ageing Report, 2023, of the 14.9 crore elderly persons in India (2022 estimates), 5.96 crore fall within the poorest wealth quintile (Sharma 2024). Further, 2011 SECC data indicates that there are 4.36 crore widows and 2.68 crore persons with disabilities. The limited coverage under the programme has led states to expand their quotas; Economic Survey of India 2024-25 acknowledges for the first time that states are providing coverage to an additional 5.86 crore beneficiaries, bringing total coverage (3.09 crore central and 5.86 crore state) to 8.95 crore (Ministry of Finance 2025).

Additionally, restrictive eligibility criteria for widows under IGNWPS and PwD under IGNDPS create further structural exclusions. The central guidelines prescribe a minimum age of forty for widows, even though economic vulnerability following the loss of a primary breadwinner may arise earlier. Further, as noted in the Mihir Shah committee report, the IGNWPS does not account for unmarried or deserted women. As a result, several states have introduced additional norms to enable their inclusion, often requiring multiple forms of documentation that are difficult to obtain, such as requirements vary by state, but may include certification from local elected representatives or authorities, or a ‘non-traceable’ police report indicating that the husband is missing.

Figure 13.2: Comparison of population estimates based on the SECC data and NSAP central caps for elderly persons, widows and PwD

For PwD under IGNDPS, the eligibility threshold remains at 80 per cent disability, whereas the Rights of Persons with Disabilities Act, 2016, recognises persons with 40 per cent and above disability for entitlement to social security benefits, leaving many eligible individuals excluded and dependent on state-level relaxations (Department of Personnel and Training n.d.; Sharma and Pathak 2025a). The eligibility framework is thus not aligned with actual vulnerability, and the requirement to furnish multiple documents places an additional burden of proof on elderly persons, widows and PwD.

13.2.3 Service delivery and flow of funds

The NSAP guidelines stipulate that an application should be processed within sixty days from receipt to sanction or rejection (Ministry of Rural Development 2014). They further require that pensions be credited monthly through DBT to beneficiary’s bank or post office accounts. With increasing digitisation, the applications are now largely submitted online through the Unified Mobile Application for New-age Governance (UMANG) portal (Ministry of Rural Development n.d.-c).

In practice, however, these provisions are rarely adhered to. The CAG’s report on NSAP (2023) notes that the sixty-day sanction timeline is routinely breached across states, leading to delays that undermine timely support (CAG 2023). Beneficiaries are often required to track their applications themselves and make multiple visits to panchayats, banks and Common Service Centres (CSCs) during the process.

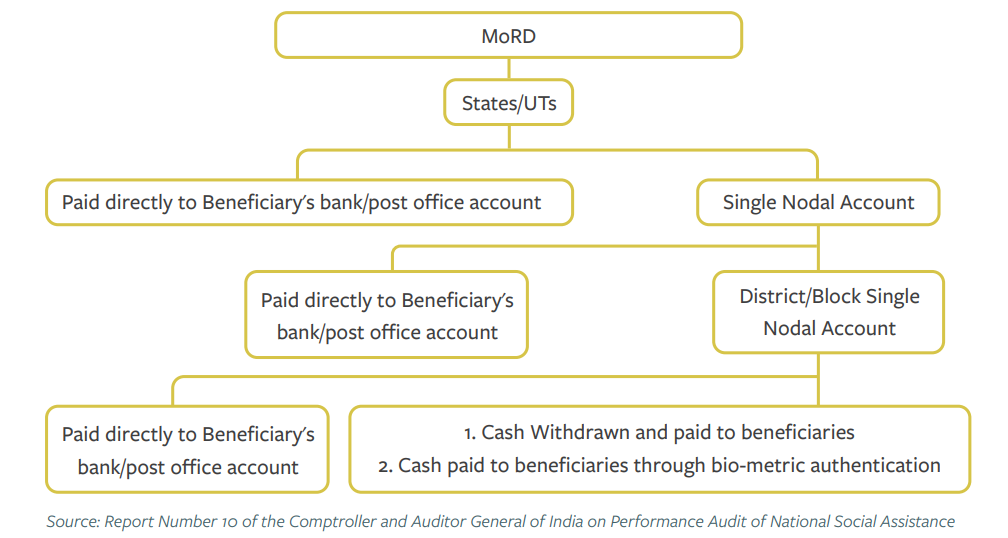

Under NSAP, pensions are disbursed through multiple channels, including bank and post office accounts, money orders and cash. As per the NSAP Management Information System (MIS) data, 87.9 per cent of beneficiaries receive pensions directly into bank accounts, reflecting the broad rollout of the DBT system. Around 4 per cent continue to be paid through post office accounts, 0.2 per cent through money orders, and 7.9 per cent — over 25 lakh beneficiaries — still receive pensions in cash (see Annexure 13.4 for the current disbursal structure). As of March 2026, twenty-two states and union territories (UTs) are DBT-compliant; however, this has not translated into regular monthly disbursal in all cases (see Annexure 13.3 for the list of DBT-compliant states and UTs).

In several states, especially Andhra Pradesh and parts of the Northeast, pensions continue to be distributed in cash due to limited banking access in remote areas. Post office accounts remain common in hilly or rural regions such as Himachal Pradesh and Odisha, where physical access is easier than banking facilities. Although states determine their modes of payment, the Centre has been pushing for DBT as the preferred method, purportedly to reduce leakages and strengthen audit trails. This shift, however, remains uneven on the ground, reflected in persistent implementation gaps in monthly pension disbursals. Payments are often made in lump-sum quarterly or biannual instalments, depending on treasury releases, undermining the purpose of a monthly social pension intended to provide consistent income support.

For example, in Delhi, 1 lakh beneficiaries faced a five-month delay due to fund-release bottlenecks, with the funds finally disbursed in August 2024 (TOI City Desk 2024). In Kerala, as of August 2025, nearly five pension instalments were pending (Sai Kiran 2025) and in Tamil Nadu, pensions are frequently credited only around the twentieth of the month (Arockiaraj 2025).

Moreover, the social audit provision is barely operational in most states. In the absence of an independent grievance redress mechanism within NSAP and with deletions not publicly disclosed, the burden falls on the applicant to pursue the state rather than on the state to guarantee continuity.

A key reason cited by the central government for delays in disbursal is states’ failure to adhere to NSAP procedures in a timely manner. However, the design of fund release and implementation—where allocations are made annually, and execution is left to state-level administrative departments such as social welfare or social justice and empowerment—also diffuses accountability (see Annexure 13.5 for scheme-wise releases to states/UTs under the three pensions schemes from 2014–15 to 2025–25).

Previously, annual allocations were released into the consolidated fund of the state or the UT in two instalments (Ministry of Rural Development 2014). The first instalment—50 per cent of the annual allocation—was released without any verification of beneficiary data or any documentation from the state. The second

Figure 13.3: Channels of payments under NSAP across states/UTs

installment was released only after the state had utilised at least 60 per cent of the total funds and upon verification through the Public Financial Management System (PFMS), which provides real-time data on fund utilisation (Ministry of Rural Development 2020). Proposals for the release of the second instalment had to be submitted by 15 December each year. From FY 2024–25, central funds are released to states in four quarterly tranches, contingent on the submission of compliance documents prior to each release (Standing Committee on Rural Development and Panchayati Raj 2025a).

Fund transfers from the Centre to states are often delayed or withheld due to non-submission of utilisation certificates and failure to submit proposals, as releases are contingent upon such documentation. As a result, funds have not been released for several years to Goa and the UTs of Andaman and Nicobar Islands, Dadra and Nagar Haveli and Daman and Diu and Lakshadweep (CAG 2023; Ministry of Rural Development 2026).

Service delivery under NSAP is presently not rooted in an entitlement-based approach. Concerns extend beyond low pension amounts and outdated eligibility criteria to the very process of delivery, which continues to treat the elderly, widowed and disabled as an applicant who must repeatedly establish eligibility, rather than as citizens entitled to social protection.

13.2.4 Union budget and increasing fiscal burden on states

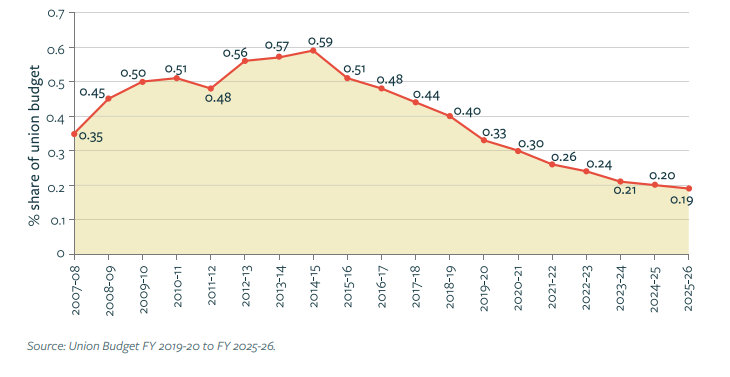

The budget allocated to NSAP by the Central government can be divided into two distinct phases: 2007–2015 and 2015–2025.

In the first phase (2007–08 to 2014–15), allocations to the programme increased alongside the expansion of the other rights-based entitlements. During this period, the budget rose from ₹2,392 crore in 2007–08 to ₹9,541 crore in 2013–14, reaching a peak of ₹10,618 crore in 2014–15. NSAP’s share of the Union budget also increased from 0.35 per cent to 0.57 per cent.

In the second phase (2015–16 to 2025–26), the programme’s budget has remained stagnant at a yearly average of ₹9,500 crore, essentially a decline in real terms. The budget has remained frozen even as economic vulnerability and postCOVID-19 shocks have persisted. Over the same period, NSAP’s share of the Union budget fell from 0.51 per cent to 0.19 per cent in 2025–26 (see Annexure 13.6 for the Union government budget for NSAP). Apart from a one-time ex gratia payment of ₹1000, amounting to ₹2,814.50 crore in 2020–21, the programme has seen no substantive enhancement (Press Information Bureau 2021).

Maintaining the same purchasing power and level of support as in 2014–15 would require allocations to increase to at least ₹18,000 crore as of March 2026, assuming an average annual inflation rate of 5 per cent (Sharma and Pathak 2025b). Fixed beneficiary caps, unrevised pension amounts for over a decade, and a policy

Figure 13.4: NSAP budget as a share of Union budget 2007–08 to 2025–06

shift towards contributory pensions schemes such as APY have together constrained the programme’s ability to provide meaningful social and economic protection, a trend reflected in its declining budget (Drèze and Khera 2016).

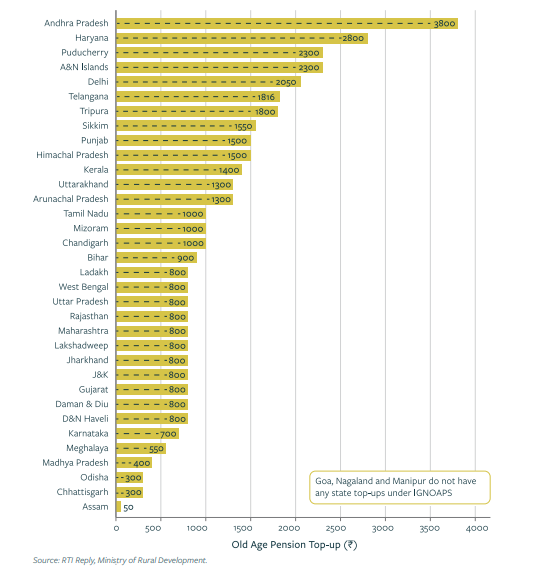

Despite being one of the six ‘core of the core’ centrally sponsored schemes, NSAP operates on a 50:50 cost-sharing ratio, unlike other schemes in this category, which typically have a higher central share,4 thereby shifting greater financial burden onto states. As a result, states face a double burden: they must not only provide substantial top-ups to compensate for the Centre’s inadequate contribution—often beyond the 50:50 ratio—but also support nearly six crore additional eligible beneficiaries who fall outside the programme’s capped list.

The scheme’s design further reinforces this shift. Low baseline pension amounts and restrictive eligibility criteria enable the Union government to rely on the programme’s federal structure to limit its responsibility for social protection. In practice, this places disproportionate administrative and fiscal responsibility on states, which must finance top-ups while also managing enrolment, verification and delivery. This has led to wide inter-state variation in both coverage and adequacy, reflecting differences in fiscal capacity. States with higher revenues, such as Andhra Pradesh, Delhi and Haryana, are able to provide higher pension amounts, whereas several smaller states like in the northeast are unable to offer even modest top-ups.

At the same time, the federal design of the scheme has also enabled states to move beyond the centre’s limited thresholds and provide more substantive social security. Many states have expanded beneficiary categories, increased pension

Figure 13.5: State and UT-wise variation in pension top-ups as per current contributions under IGNOAPS

amounts, and strengthened delivery mechanisms beyond the scope of NSAP guidelines. As a result, despite limited central spending on social protection, states with political will and fiscal capacity have been able to build more comprehensive pension systems.

13.2.5 Newer architectures of exclusion

Across India’s welfare programmes, the state’s increasing dependence on techno-governance has reshaped the nature of exclusion. Systems introduced to streamline delivery and improve oversight have instead created fresh barriers to access within NSAP.

- Layers of digital payment

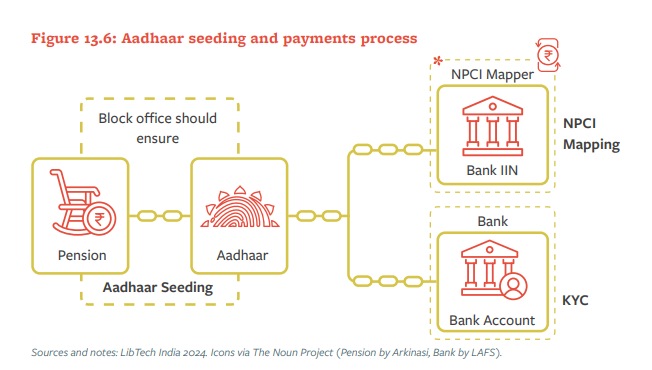

Service delivery under NSAP, like other welfare schemes, is anchored in DBT (see Annexure 13.8.1 for steps for linking Aadhaar to bank accounts and to the National Payments Corporation of India (NPCI) mapper), which is increasingly linked to the Aadhaar ecosystem. Unlike other welfare schemes, where the Aadhaar-based Payments Systems (ABPS) has been made mandatory, under NSAP, Aadhaar linking for DBT is ‘encouraged but not mandatory’ (RTI reply from the Ministry of Rural Development, 2025). Despite the Supreme Court’s ruling that Aadhaar cannot be made mandatory for welfare delivery, there has been a continued push to link DBT with Aadhaar. This has resulted in an increase in Aadhaar-related errors, including seeding discrepancies and problems with Aadhaar mapping on the NPCI platform (Sikri 2015).

According to the CAG report, the integration of PFMS with DBT since 2017 has led to issues such as name mismatches and faulty account mapping, resulting in disruptions in pension payments (CAG 2023). Since 2020–21, the government has also pushed Aadhaar seeding with pension-linked bank accounts as a means of verifying beneficiary details. Under this process, Aadhaar and bank account details are matched with the Unique Identification Authority of India (UIDAI) database, after which Aadhaar can function as the primary identifier for DBT. However, errors often occur at this stage, including incorrect data entry and mismatches in names, addresses, or age. These discrepancies can lead to authentication failures, rejected payments, or wrongful discontinuation of pensions.

More recently, an additional layer of Aadhaar seeding—linking Aadhaar to the beneficiary’s bank account and updating this information in the NPCI mapper— has emerged as another source of exclusion. Under the ABPS, DBT payments can be processed only after a multi-step process is completed. Banks must first complete e-KYC, authenticate Aadhaar, and upload the linkage to the NPCI mapper; the NPCI must then verify and update this information in its system.

This Aadhaar-NPCI linking step is often outside the control or knowledge of the beneficiary and informed consent is frequently bypassed when placing or over- riding a customer’s bank account in the NPCI mapper. Since the mapper determines which single bank account will receive all DBT payments, any unilateral change made by one bank can override another existing mapped bank account. Beneficiaries with multiple Aadhaar-linked accounts become particularly vulnerable as the mapper defaults to the most recently KYC-updated account. As a result, pensions may be redirected to dormant or inactive accounts (Kodali 2020).

Even when a beneficiary’s Aadhaar is correctly seeded in both the scheme database and the bank, payments may still be rejected if the bank fails to push the correct Aadhaar–account linkage to the NPCI mapper, often leaving beneficiaries without any means of redress, resulting in opaque processes and untraceable decision-making (Sharma and Pathak 2025a).6 Additionally, seeding, authentication, and mapping are three distinct processes managed by different institutions, including state pension departments, UIDAI and NPCI. According to the NSAP MIS (as of March 2026), of the total 2.97 crore pensioners under the programme, Aadhaar for 2.64 crore beneficiaries (88.78 per cent) was linked in the database, but Aadhaar for only 1.12 crore beneficiaries (37.94 per cent) was mapped on the NPCI mapper, potentially leaving lakhs of eligible beneficiaries vulnerable to losing access to their pensions despite having fulfilled all other requirements (Ministry of Rural Development n.d.-d).

- Additional layers of digitisation and algorithmic exclusions

The expansion of digital systems at both the central and state levels has become another major driver of exclusion within NSAP pension schemes. As states roll out their own platforms, such as Haryana’s Family Identity Data Repository or Rajasthan’s RajSSP, data inconsistencies between these systems and the central database have grown (Tapasya, Sambhav and Joshi 2024). Because these platforms do not consistently communicate or synchronise updates, basic details such as gender, name spellings, or personal information are often recorded incorrectly.7

Introduced in 2020 by the Haryana Government, the Parivar Pehchan Patra (Family ID) is a database that uses algorithms and AI to determine beneficiary eligibility and link individuals to welfare schemes. Its implementation has resulted in thousands of NSAP beneficiaries in Haryana being wrongly declared dead, leading to the stoppage of pensions and other welfare benefits (Sambhav, Tapasya and Joshi, 2024)

These examples illustrate how technology-driven systems are producing new forms of exclusion within NSAP. At the same time, the landscape of digitisation continues to evolve, new requirements and procedural changes routinely introduce additional barriers. For instance, since 1 April 2023, the Central government has made it mandatory to provide a Unique Disability ID (UDID) number or enrolment ID to access benefits under seventeen centrally supported schemes, including scholarships, health insurance programmes, and NSAP. Although intended to streamline processes and reduce paperwork, this requirement has, in practice, excluded many disabled beneficiaries from the system.

Similarly, periodic physical verification at the block level requires elderly, widowed, or disabled applicants to repeatedly present themselves or their documents to remain ‘active’ in the database. If Aadhaar seeding fails, biometric authentication does not match, or a bank account becomes dormant, pensions stop without warning. There is no mandatory human override, no institutionalised second check and no provision for home-based verification for bedridden individuals. These gaps point to a structural failure to accommodate those most at risk of exclusion through digital processes without corresponding accountability mechanisms (Sharma and Pathak 2025a).

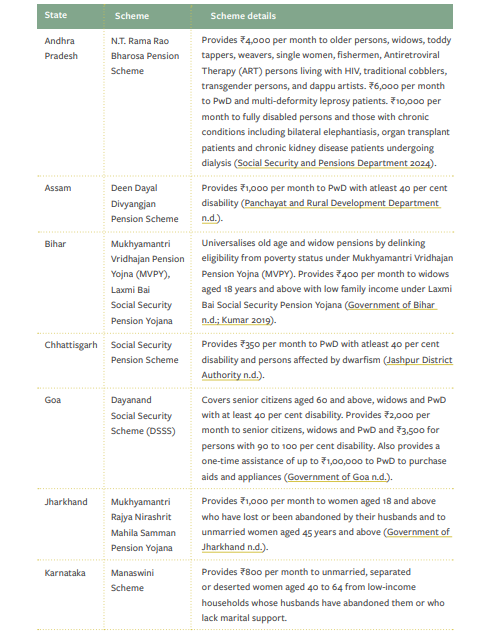

13.3 Best practices from States

The shifting of the welfare burden onto states has led them not only to contribute more funds but also to undertake major reforms to strengthen old-age and social security pensions. These reforms include improving delivery systems and widening eligibility to close coverage gaps and enhance inclusion beyond the prescribed guidelines.

Table 13.1: State initiatives expanding coverage and eligibility in noncontributory pensions

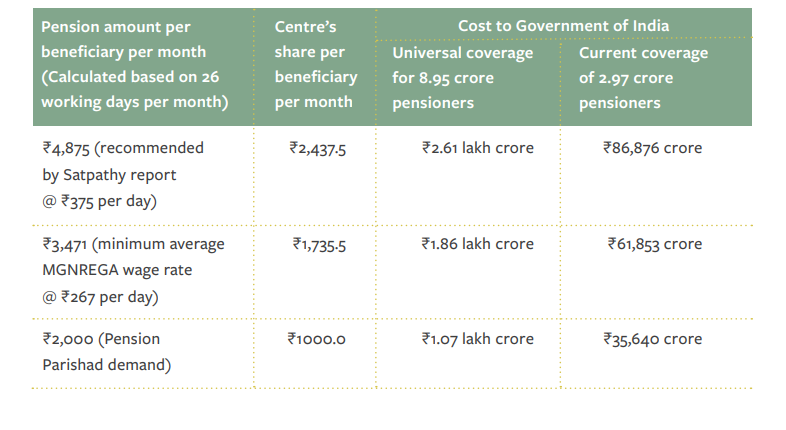

Table 13.2: Comparison of estimated costs under universal coverage and current coverage scenarios across different pension amounts

13.4 Towards a meaningful social security pension system

The systematic underfunding and undercoverage of NSAP have made it one of the most neglected pillars of India’s social security architecture. The civil society campaign advocating for social security pensions, the Pension Parishad, has long argued that, for social assistance to be meaningful, pensions should be universalised, with amounts set at 50 per cent of the minimum wage and adjusted annually for inflation so that the value of assistance does not erode over time.

However, the argument for universalisation is often rejected within dominant policy frameworks, largely shaped by the World Bank’s advocacy for targeted welfare systems and safety nets, which hold that benefits should be directed to the poorest through ‘means tests’. Despite extensive research demonstrating that targeted approaches are highly exclusionary, often marked by significant ‘targeting errors’, stigma, and administrative burdens that prevent eligible individuals from accessing support, the case for universalisation in India is routinely dismissed as fiscally unviable (Patel and Midgley 2023).

Yet even a modest attempt to meet existing needs reveals the scale of fiscal neglect. At the current assistance of ₹200 per month, covering all 8.95 crore eligible beneficiaries would raise the NSAP budget to more than ₹21,000 crore, far above current Union government allocations. However, if the government were to apply the minimum wage principle, based either on the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) average daily wage rate (₹267 per day) (Ministry of Rural Development n.d.-a) or the recommendations of the Anoop Sathpathy Committee (₹375 per day) (Ministry of Labour and Employment 2019), the required allocation would increase to ₹1.86 lakh crore and ₹2.61 lakh crore, respectively. Even raising the pension modestly to ₹2,000 per month would require the union government to allocate over ₹1.07 lakh crorecrore. This underscores how far current budgetary provisions fall short of providing even a basic level of income security.

The argument for a stronger non-contributory social assistance programme is not only political or moral but also economic. Direct income support boosts consumption and provides a basic buffer against economic shocks, especially for those with the least savings and highest vulnerability. Moreover, in a country marked by high levels of inequality, directing resources, both in cash and kind, as forms of social assistance not only reduces immediate poverty but also contributes to addressing long-term structural inequalities.

More importantly, the NSAP must be understood as part of a broader rightsbased framework of the state, similar to other entitlements secured through legislation, such as the right to work under MGNREGA and the right to food under the NFSA. Unlike MGNREGA and the NFSA, however, the NSAP lacks the statutory and legal backing afforded to other social security entitlements (Sharma 2024).

Recognising this gap, and following sustained on-ground advocacy by groups such as the Suchna Evam Rozgar Adhikar Abhiyan and the Mazdoor Kisan Shakti Sangathan, the government of Rajasthan enacted the Minimum Guaranteed Income Act in 2023—the first law of its kind to provide a legal and enforceable entitlement to inflation-indexed social security pensions. Therefore, for the social assistance programme to fulfil its intended function, the NSAP requires comprehensive restructuring. A meaningful and robust social security architecture would require:

i. Pension amounts must be revised upwards to at least half of the minimum wage and periodically adjusted for inflation so that the real value of assistance does not erode over time;

ii. Similar to a national minimum floor wage, a national minimum pension must be established to ensure greater parity across states, where beneficiaries in one state may receive as little as ₹200 while those in another receive up to ₹5,700;

iii. Coverage must be broadened beyond outdated caps tied to the 2001 Census and, at the very least, aligned with the 2011 SECC data until fresh census data become available; and

iv. Social assistance must be grounded in a statutory and justiciable framework so that entitlements are enforceable as rights rather than contingent welfare provisions, thereby ensuring accountability and moving towards universalisation so that no eligible person is excluded.

In the absence of fiscal, legal and normative reforms, the programme will continue to remain largely symbolic, falling far short of even a minimal level of income security. In a country where nearly 90 per cent of the workforce is employed in the unorganised sector and receives no post-retirement security, the NSAP must be recognised as the primary guarantor of a minimum income in old age, widowhood and for persons with disabilities. Social security pensions, therefore, are not discretionary welfare transfers but form part of the minimum rights guarantee framework, constitutionally mandated for dignity and survival (Drèze and Sen 1991).

This is a chapter from, Realising Rights: A Handbook of Welfare in India, published by the Centre for the Study of the Indian Economy, Azim Premji University. Read and download the full handbook here.