Introduction

Introduction

The global economy is in a downward trend, fuelled by the third wave of the pandemic. In India, the role of Public Sector Banks (PSBs) which constitute more than 65% of the banking system, is critical to slow down this trend and reduce the impact on the economy, as seen during the 2008 economic crisis. The need of the hour is to strengthen the banking sector, which is the real backbone of Indian Economy.

This article specifically covers the factors faced by the Indian Banks in the part of their poor NPA management in the past six years, especially due to the implementation of stringent NPA provisioning norms and capital norms from the regulators followed with favourable guidelines supporting the Defaulters under NCLT/IBC cases. This article in depth furnishes the data of all Scheduled Commercial Banks (SCB) – category wise (Public Sector, Private Sector, Foreign banks & Small Finance banks) towards how many actual recoveries are made against the slippages and how much write-off/prudential write-off made which has only played a dominant role in the computation of arriving the overall gross NPAs into a reduced position.

Reasons for major crisis under NPA management of PSBs

The following factors are the main reasons for the crisis in the banking sector.

- Due to the economic slowdown, the gross NPAs started increasing from 2015 itself, and are still persisting. Certain stringent policies by the RBI regulators added fuel to the fire.

- The abnormal NPA provisions are made as per the NPA provisioning policies with the assurance and the strength of capital infusion to off-set / adjust the P&L loss incurred. So, PSBs made huge write-offs and this affected 100% provisioning. An unhealthy prudential write-off was made, which reflected poor Net Advances position under the Balance Sheet.

- PSBs have been incurring losses since 2015-16. It’s only in 2020-21, PSBs reported a net profit of Rs.31818 cr. Because of huge NPA provisions, earlier they incurred a net loss. But, they have shown sizable operating profits (profit before provisions) all over the period. NPA provisions are more than the gross profit for all the last five years (peak in 2017-18, 2018-19 & 2019-20). For NCLT accounts, haircuts are more than 90%. For any Write-off accounts, NPA provisions are to be made 100%. Entire provisions are made strictly as per the RBI guidelines. In 2020-21, write-offs have come down because no new entries are allowed to include in NCLT/IBC as per SC directives due to corona impact.

- Since the computation of gross NPAs is subject to deduction of all write-offs made every year, the accounting of gross NPAs have sizably come down. Write-off and NPA provisions are mutually interlinked. The income on advances has been much impacted, which has led to a reduction in operating profits.

NPA Management and basic concepts

RBI issues detailed guidelines to banks on the method of arriving NPAs for each category of advances and also fix the provisioning norms for different segments of NPAs, and it is revised from time to time. In the books of banks, a non-performing asset (NPA) is a loan or advance for which the principal or interest payment remained overdue for a period of 90 days. It is different for agricultural advances. Again, banks are required to classify NPAs further into Substandard, Doubtful (D1:<1 year, D2:1 to 3 years, D3:>3 years) and Loss assets. Substandard assets are those who have remained NPA for a period of less than or equal to 12 months. Doubtful assets are those assets that have remained in the substandard category for a period of 12 months. The Loss assets are considered uncollectible and of such little value that its continuance as a bankable asset is not warranted, although there may be some salvage or recovery value. Since 2014, RBI further classified Special Mentioned Accounts (SMA), which are those assets/accounts that show symptoms of bad asset quality in the first 90 days itself. In the case of SMA 1, the overdue period is between 31 and 60 days, and it is 61 to 90 days for SMA 2.

What is Writing-Off NPAs & Technical Write-off?

In terms of Section 43(D) of the Income Tax Act 1961, income by way of interest in relation to bad and doubtful debts shall be chargeable to tax in the previous year in which it is credited to the bank’s profit and loss account or received, whichever is earlier. This stipulation is not applicable to provisioning required to be made as indicated above. In other words, amounts set aside for making provision for NPAs as above are not eligible for tax deductions. Therefore, the banks should either make full provision as per the guidelines or write-off such advances and claim such tax benefits as are applicable, by evolving appropriate methodology in consultation with their auditors/tax consultants. Of course, recoveries made in such accounts should be offered for tax purposes as per the rules.

Banks may technically write off advances at the Head Office level, even though the relative advances are still outstanding in the branch books. However, it is necessary that provision be made as per the classification according to the respective accounts.

Thus, the bank makes a list of all such NPA accounts (gross NPAs) and makes NPA provisions as per RBI guidelines revised from time to time. Such provisioning % also varies as to the different categories of NPAs.

Banks show more interest in vouching for write-off and technical write-off to benefit some interest gains/reversals as per the exiting Income tax regulations. Hence, Bank’s official data on the present gross NPAs are computed after deducting huge general write-off and prudential write-off only. RBI guidelines allow them to do so. To meet this, huge NPA Provisions are made, which affects the profitability of banks directly. Almost all the rating agencies, in general, talk much about the slippages, recoveries, restructure but less about the write-off.

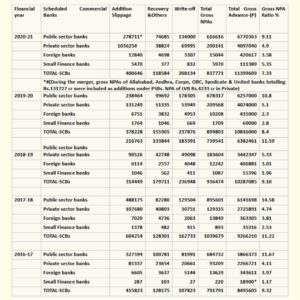

Hence, in our Banking System, the gross NPA ratio, as well as the gross NPA value, mainly comes down because of huge write-offs than the other key factors like rescheduling and actual recoveries. The following table substantiates the same.

Status of NPAs

Our own consolidation (from the RBI Statistical data released) on the movement of NPAs 2014-15 to 2020-21 is given below: (Rs.in cr)

^^ PROVISIONAL FIGURES –(P)

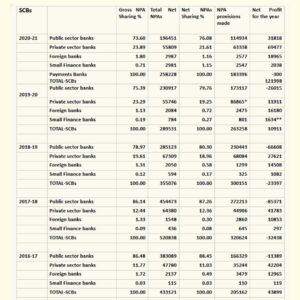

Also, PSBs incurred huge losses mainly because of abnormal NPA provisions (due to write-off adjustments) as per the table given below:

*Yes bank alone Rs.27806 cr **include Payments banks loss of Rs.304 cr (Our own consolidation from the data published Statistical Tables Relating to Banks in India: 2020-21)

Also, it is clear that more than 30% of total gross NPAs are made into NPA provisions every year and more than 25% of gross NPAs are made into write-offs every year in order to reduce the gross NPAs.

Conclusion

As such, in reality, the major NPAs have been washed out by huge write-offs. The entire banking system is pilfering public money in the form of haircuts and write-offs, mainly letting the corporate giants gain more and more benefits due to the favourable norms and policies regulated and implemented for them. The banks should publish their sector-wise write-off amounts for greater transparency and accountability.

Centre for Financial Accountability is now on Telegram. Click here to join our Telegram channel and stay tuned to the latest updates and insights on the economy and finance.