RBI has released draft Directions for “Relief Measures in Areas Affected by Natural Calamities,” the Reserve Bank of India (RBI) seeking to rationalise and harmonise prudential norms governing loans disrupted by calamities and other events. These Directions, issued ostensibly after the RBI’s June 8, 2023 policy statement, aim to replace multiple existing circulars — including the 2018 Master Directions — with a framework applicable to banks, non-bank lenders, and cooperative institutions. The directions will be implemented from April 1st, 2026.

On the surface, the attempt to clarify scope, unify regulatory expectations, and prescribe procedural timelines is welcome. In recent years, climate-related disasters have grown in frequency and intensity, inflicting deep socio-economic harm across regions. Courts and civil society have repeatedly underscored the need for substantive relief for disaster-hit borrowers; in the Wayanad landslide case, for instance, the Kerala High Court observed that compelling survivors to service agricultural loans when their collateral no longer exists was an affront to dignity protected under Article 21. Civil society organisations, after the devastating 2025 monsoon floods, jointly appealed to the Union Government and financial regulators for urgent, comprehensive relief. These developments reflect a growing recognition that finance policy has social consequences far beyond balance sheets.

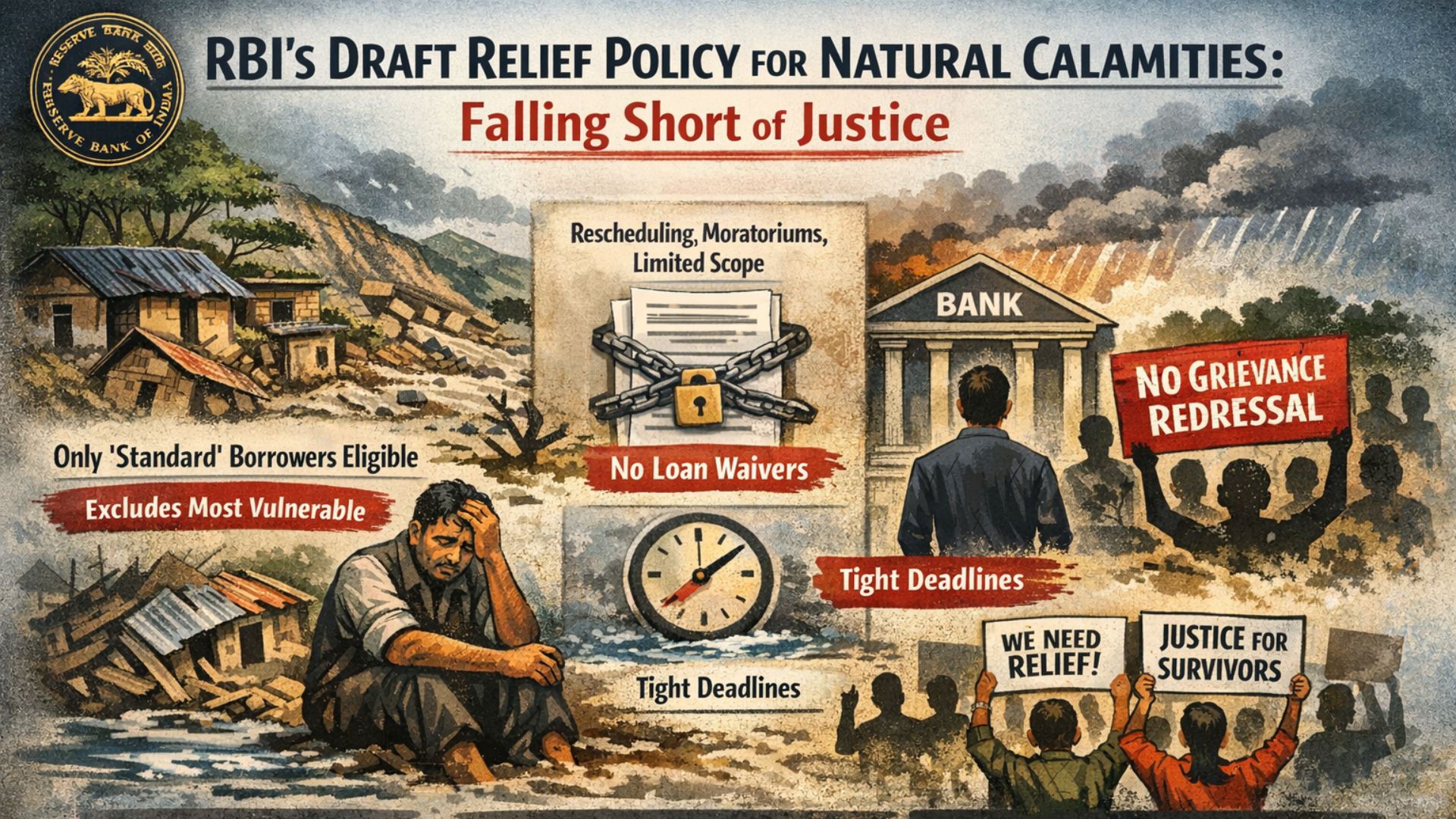

Yet, despite its procedural recommendations, the draft Directions ultimately fall short of delivering the justice that disaster-affected populations need. At heart, the framework reflects a prudential lens that prioritises bank asset quality over people’s lived realities.

A central flaw lies in the exclusionary eligibility criteria. Relief under the framework is limited to borrowers whose accounts are classified as “Standard” and who are not in default for more than 30 days at the time the calamity struck. In practice, this means only those with perfect repayment histories — often relatively better-off borrowers — qualify. In disaster-prone regions marked by agrarian distress, irregular incomes, and repeated climate disasters, even minor delays in repayment are common. By tying relief to ‘good’ repayment behaviour, the framework systematically excludes precisely those borrowers most vulnerable to climate disasters.

Equally concerning is the limited ambit of permissible resolution tools. The Directions allow rescheduling of payments, conversion of accrued interest, moratoriums, and, at best, additional credit — measures that offer temporary breathing space but do little to address deep and enduring losses. Nowhere does the framework mention loan waivers or principal write-offs as remedies for a disaster resolution plan. Relief — such as fee waivers — is left entirely to bank discretion. This narrow conception of relief risks turning “resolution” into postponement of distress, rather than a meaningful reset for borrowers whose livelihoods have been obliterated by calamities.

Critically, the architecture of the framework also vests excessive discretion in lenders without adequate safeguards for borrowers. Resolution must be invoked within 45 days of a calamity declaration and implemented within 90 days. While timelines are important, they may be unrealistic in the aftermath of large disasters, when documentation, damage assessments, and borrower outreach are severely constrained. Although a one-time extension can be sought, there is no robust mechanism acknowledging on-the-ground administrative and social realities that may pose a challenge to compliance with procedural deadlines.

Worse still, the draft does not institutionalise any mechanism to recognise or respond to public and civil society demands for loan relief — even though such demands have historically crystallised in the wake of disasters. Loan relief is not merely an individual banking decision; it is a collective socio-economic concern. Yet the Directions lack any provision for consultation, transparency, or disclosure of relief decisions to affected communities, thereby weakening democratic accountability.

The framework does not establish a dedicated grievance redressal mechanism specific to calamity-related resolutions. Given the discretionary powers conferred on lenders, borrowers must have access to grievance redressal at both bank and RBI regional office levels to challenge exclusion, delays, or denial of relief – a safeguard conspicuously absent in the current draft.

To be sure, there are some positive elements – such as the requirement for lender policies on dealing with calamities and the provision allowing restructuring without waiting for insurance settlements, which are often delayed and uncertain. Mandated reporting on the RBI’s monitoring portal could enhance transparency, provided the data is publicly available.

For the RBI’s framework to meaningfully address disaster-induced indebtedness, it must move beyond narrow prudential concerns. Eligibility must be broadened; resolution tools must include waivers where appropriate; and transparent, participatory grievance redressal mechanisms must be built in. Above all, regulatory policy must recognise that financial distress in calamity-hit regions is not a technical problem but a deeply social one – demanding compassion, accountability, and justice.