TO PROTECT HARD EARNED SAVINGS OF THE COMMON MAN

ORIGIN OF DEVELOPMENT BANKING

Historically, the idea of establishing special institution for the provision of finance for industry was put forth in strong terms, as far back as 1931, by the Central Banking Enquiry Committee. The Committee recommended the creation of Provincial Industrial Credit Corporations and an All India Institute for the purpose of catering to the financial needs of regional and national importance respectively. In May 1945, RBI undertook detailed study whereby it was recommended that there is a need to form specialized institution at both all India level and regional level to cater to Industrial Finance. Accordingly the first institution was established in 1948 called Industrial Finance Corporation of India. This was the beginning of development banking in India.

BIRTH OF IDBI

In 1947 India became independent. In 1950 India became Republic and adopted the path of planned economy by launching first Five Year Plan with focus on development of Core Sector and Infrastructure Industry to make India self-reliant. This was possible only with the huge investment in private as well as in public sector but private sector was reluctant since this investment was huge and long term bearing high risk. This was pursued by the government in successive Five Year Plans but since there was no significant progress ultimately government decided to form IDBI as wholly owned subsidiary of Reserve Bank of India (RBI) to dedicatedly pursue the cause.

IDBI was formed through an enactment of the parliament in 1964 with a purpose to have broad based industrial development as a part of national policy. The fundamental objective of setting up of IDBI as stated by the then Finance Minister of Government of India Mr. T.T. Krisnamachari was:-

“We are envisaging the new Industrial Development Bank of India as a Central Coordinating Agency which ultimately will be concerned, directly or indirectly with all the problems or questions relating to the long and medium term financing of Industry and will be in a position, if necessary, to adopt and enforce a system of priorities in promoting future industrial growth.”

DEFINED ROLE OF IDBI

IDBI was also entrusted with the role and responsibility of acting as the ‘Principal Financial Institution’ engaged in financing, promotion and development of industry so as to remove regional disparities in the growth and development. IDBI has provided assistance to development related projects and contributed in building up substantial capacities in all major industries in India. IDBI has directly or indirectly assisted all companies that are presently reckoned as Major Corporate in the country. It has played dominant role in balanced Industrial Development.

IDBI was asked to finance long term projects, big projects which normally commercial banks were no more interested to finance since repayment period was for a long tenure thus leading to asset liability mismatch. IDBI was also asked to provide support and assistance to State Level Financial Institutions by providing refinance as also requisite skill to give impetus to the Industrial Development in the backward areas.

In order to facilitate to discharge this role and responsibility, IDBI was being provided low cost funds by the government of India through RBI {Long Term Operations Fund} SLR Bonds, Investment Deposit Accounts {IDAS}, Capital Gains Bonds etc., and was given tax free status which subsequently helped the institution to fulfill the national objectives and role assigned to the bank in the economy.

CHANGING FACE OF IDBI AFTER 1991 REFORMS

IDBI setup Small Industries Development Bank of India (SIDBI) as wholly owned subsidiary to cater to specific needs of Small Scale Sector in 1990. IDBI has engineered the development of capital market through helping in setting up of the Securities Exchange Board of India (SEBI), National Stock Exchange of India (NSE), Credit Analysis & Research Ltd (CARE) and Stock Holding Corporation of India Ltd (SHCIL), Investor Services of India Ltd (ISIL), National Securities Depository Ltd (NSDL) and Clearing Corporation of India (CIL). IDBI became first All India Financial Institution to obtain IS0 9001 Certification. In 1982, International Financial Division of IDBI was converted into Export Import Bank of India (EXIM Bank) wholly owned Corporation of Government of India under an Act of Parliament. In December 1993, IDBI setup IDBI Capital Markets Services Ltd as a wholly owned subsidiary to offer wide range of financial services including Bond Trading, Equity Broking, Client Assessment, Management and Depository Services. In March 2000, IDBI set up IDBI Intech Ltd as wholly owned subsidiary to undertake IT related activities. In March 2001, IDBI setup IDBI Trusteeship Services Ltd to provide technology driven information and professional services to subscribers and issuers of debentures, strategic management of Non Performing Assets and Stressed Assets of financial institutions and banks. In 2003, IDBI acquired entire shareholding of Tata Finance Ltd in Tata Home Finance Ltd, which subsequently was renamed as IDBI Home Finance Ltd. Thus it can be seen that IDBI has played important role in industrial development and development in finance and capital in general.

In 1991, as a sequel of New Economic Policy, Indian Government adopted the path of New Banking Policy to be in tune with New Economic Policy, which is popularly known as “Narsimham Committee Recommendations” which in its Report II states as under:-

- Development Financial Institutions (DFIs) should over a period of time convent themselves into Banks failing which it will be converted as Non Banking Finance company.

- DFI which converts into Bank will be given time to comply with reserves requirement of its liability at par with commercial bank.

- SIDBI be delinked from IDBI & IDBI be converted into joint stock company in terms of Indian Companies Act to provide flexibility in its operations.

In consonance with the above recommendations IDBI set up IDBI Bank Ltd in association with SIDBI as a subsidiary Private Sector Commercial Bank, as sequel to RBI’s policy of opening up of domestic banking sector to private participation as a part of overall financial sector reform. In October 1994, IDBI Act was amended to permit public ownership up to 49%. In July 1995, IPO of equity to raise Rs. 2000 Crores was issued to reduce government stake to 72.4%. In June 2000, part of government shareholding was converted to preference capital since redeemed in March 2001 thereby government’s stake was further reduced to 58.47%.

With the advent of new Banking Policy framework as provided by the Narsimham Committee recommendations, the concessions provided to IDBI in the form of tax exemptions and mobilization of funds at cheaper rate was withdrawn to have level playing field. This ultimately pushed IDBI from Development Banking to Commercial Banking to have access to relatively cheaper funds in the form of Savings & Current account deposits.

IDBI ACT REPEALED– END OF DEVELOPMENT BANKING IN INDIA

On 16th December, 2003 parliament approved the IDBI (Transfer of Undertaking and Repeal Bill) 2002 to repeal IDBI Act 1964. The repeal act aimed at bringing IDBI under Companies Act to enable operational flexibility to undertake Commercial Banking business under Banking Regulation Act 1949, in addition to the business carried out by it under IDBI act 1964. It is pertinent to note that during the debate on the bill the then Hon. Finance Minister Shri Jaswant Singh assured the Lok Sabha on 8th December 2003 that IDBI shall retain its Development Financial Institution status even after its conversion into deemed banking company and Government of India shall at all the times hold not less than 51% of the capital. This assurance was taken on record by the Parliamentary Committee on Government Assurances and precisely with these this bank was being categorised as Other Public Sector Bank by the Reserve Bank of India. On 29thJuly, 2004 the Board of IDBI and IDBI Bank Ltd took in-principle decision regarding merger of IDBI Bank Ltd with proposed IDBI Ltd. The new entity Industrial Development Bank of India was incorporated on 27th September, 2004 and Certificate of Commencement of Business was issued by the Registrar of Companies on 28th September, 2004. In September 2004, its NPA amounting to Rs. 9000 crores were transferred to a trust – ‘Stressed Asset Securities Fund’ to reduce NPA from 12% to 2% to clean the balance sheet while the new entity was to be put into operations. Government issued notification on 29th September, 2004 to operationalize the new entity with effect from 1st October, 2004. RBI also issued notification for inclusion of IDBI Ltd in schedule II of RBI. Thus, this was the end of development banking in India.

WHO IS RESPONSIBLE FOR THIS DESTRUCTION?

This is how a dedicated institution for Core Sector and Infrastructure Finance with huge in amount and long term in nature was dispensed with and with this all those sectors started approaching different Commercial Banks for whom appraisal of projects and technical feasibility were new concepts. All those commercial banks were mobilising funds for a short term period and lending for long term, leading to asset liability mismatch. Some of the projects were stuck up due to want of various permissions resulting into cost escalations and resultantly those projects became unviable while some of the projects were stuck up in legal battle resulting into accounts becoming NPA. At the same time cronies by using their acquaintance with the ruling class, in connivance with the top bureaucrats from banks, RBI and Ministry of Finance have availed huge finances and have directed the same for the purpose other than for which the same was lent, resulting into huge NPA’s. Initially those accounts were restructured by resorting to the RBI guidelines in this behalf but consequent upon Asset Quality Inspection by RBI at the instance of the then RBI, Governor, Mr. Raghuram Rajan all those NPA’s were unfolded leading to the present crisis in banking including IDBI, which in case of IDBI was still deeper since it had legacies of corporate debt.

MOUNTING NPA: – ROOT CAUSE FOR THE PRESENT CRISIS

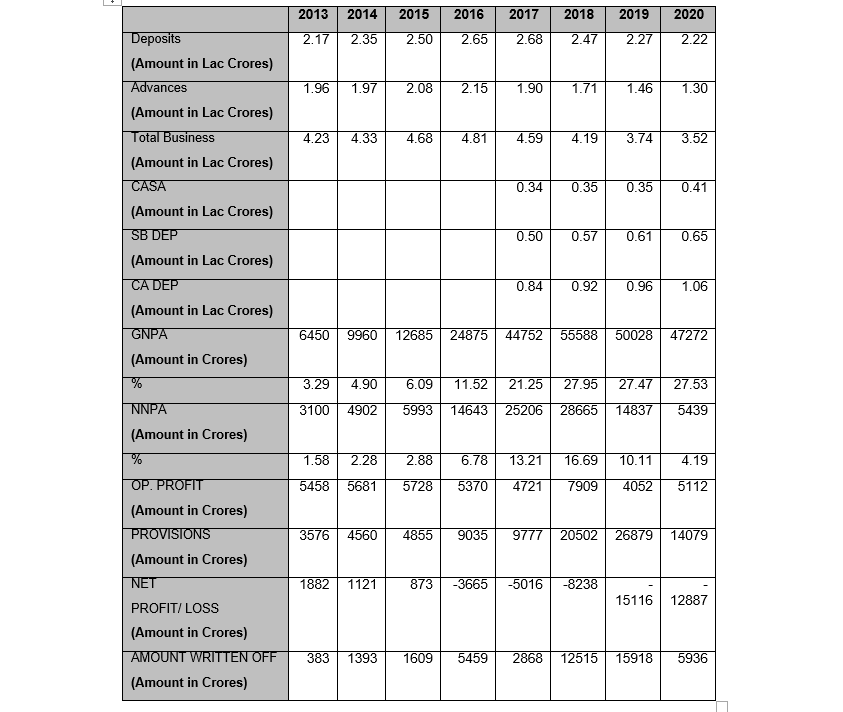

In 2004, after transfer of about Rs 9000 crores of NPA to the Stressed Asset Structured Fund, NPA level of IDBI was brought down to 2% but now, as of March 2019, once again it has reached to an all-time high and highest in banking industry at 27.49% i.e. Rs 50,028 crores because of which IDBI has incurred losses continuously for the last four years and therefore this bank was brought under the Prompt Corrective Actions (PCA). Huge NPA coupled with rampant corruption in high offices is also the reason government was required to infuse capital amounting to Rs. 23,227 crores in last five years to comply with the regulatory capital requirement in IDBI. This capital is also eroded due phenomenal growth in NPA and continued huge losses.Thus bank had to face constraints in lending and as sequel effect it had to stop mobilising deposits and precisely this is the reason for shrinking its balance sheet from Rs 4.23 lac crores in 2012-13 to Rs 3.70 lac crores in 2018-19.

In order to overcome this crisis, IDBI needs capital which government was unable to provide in budget since it would have resulted either in widening the budget deficit or additional taxes. To overcome this Government of India resorted to divest its ownership by selling off its stake to LIC who by infusing Rs. 4,743 crores has acquired 51% stake in capital which means the ownership of IDBI in the year 2019 stands transferred to LIC from Government of India. Thereafter RBI has come out with the notification that hereafter IDBI will be classified as Private Sector Bank for the purposes of regulator which government claims that since LIC is public sector, IDBI will continue to have status of Public Sector in its character.

IDBI: – BUSINESS PROFILE

Even though IDBI was converted into commercial bank it was expected of the bank to continue to perform the role of credit to long term projects & big projects. The Dabhol Power Project is the live example of it. Initially IDBI had assessed the project as unviable but the government in its capacity as owner asserted with the bank to lend. Ultimately this project failed for various reasons and entire buck was passed on to IDBI. This example is not in isolation but many more such projects were imposed on IDBI of which some have failed due to sluggish growth of the economy, litigations in Supreme Court, willful default, financial frauds by the borrowers etc., resulting into piling up of huge NPA’s which were unfolded more particularly consequent upon Asset Quality Inspection initiated by RBI at the instance of the then Governor of RBI Mr. Raghuram Rajan which accounts till then were being shown as performing in the books of accounts of the bank by restructuring them in terms of RBI guidelines only.

All those NPA accounts is the creation and resultant effect of policies implemented by the government from time to time but now the whole buck is being passed on to IDBI as if it is the creation of the Bank. All those NPA accounts are pending before NCLT, DRT, DRAT etc., in which either disposal is taking too much time or IDBI is required to take hit on its bottom lines in the name of haircut.

IDBI PASSING THROUGH TOUGH TIMES

Presently IDBI Bank is passing through tough times mainly on account of huge NPA’s. Growth in Gross NPA of IDBI Bank from Rs. 6,450 crores in 2013 to Rs. 47,272 crores in 2020 is 7.32 times. This figure is excluding Write Off of bad debts amounting to Rs. 35,182 crores. Thus bank has incurred losses continuously for the last five years.

It is therefore that the government was required to infuse capital repetitively. Government has infused around Rs. 23,227 crores capital in IDBI in the last seven years and now again government has infused Rs. 4,557 crores capital while LIC has infused Rs. 4,743 crores capital to bailout ailing IDBI. In the year 2017, RBI came out with new template of Prompt Corrective Actions (PCA) which was imposed on IDBI in May 2017 because of which IDBI was unable to lend and it is therefore that IDBI is not keen in mobilizing deposits. Thus the journey of development banking was converted into commercial banking and thereafter this bank was corporatized and now its ownership is being transferred to LIC, a Public Sector Financial Institution from Government of India and now much is being said on its privatization which for all practical purposes will be an end of great IDBI.

IT IS THE BIG BUSINESSES WHO SPOILED IDBI !

DEBT RECOVERY TRIBUNAL: – FAILED ATTEMPT

In the initial stages of reforms in the year 1992-1993, after identification of NPA for the first time, government came out with Debt Recovery Tribunals instead of Civil Courts to expedite legal proceedings in the NPA accounts with balance above Rs. 10 lacs. IDBI has initiated legal proceedings against 4,269 borrowers with an amount outstanding of Rs. 38,473 crores in DRT of which 3,687 cases are pending since long in various DRTs with an amount outstanding of Rs. 35,263 crores i.e. 91%.

BANKRUPTCY CODE: – GREAT ILLUSION

IBC: – ESCAPE ROUTE FOR THE CORPORATE

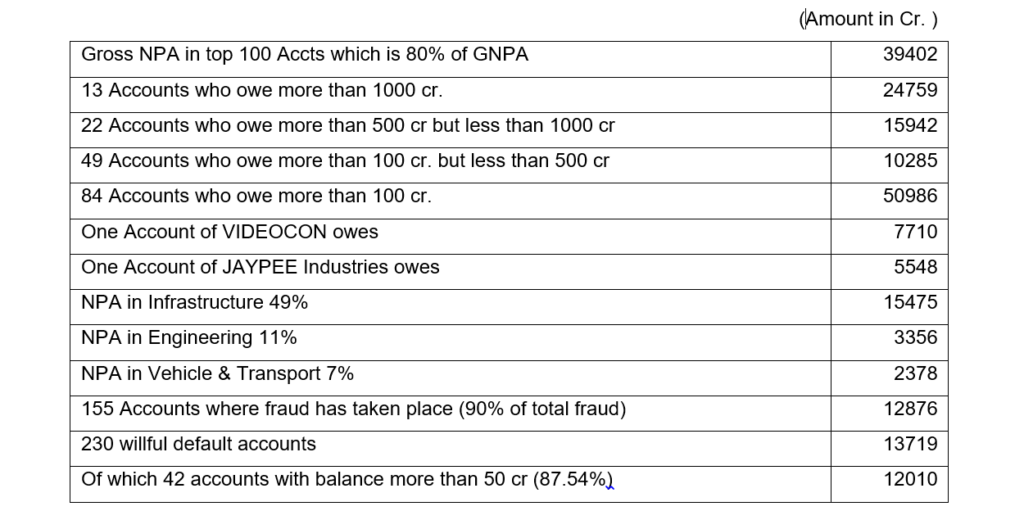

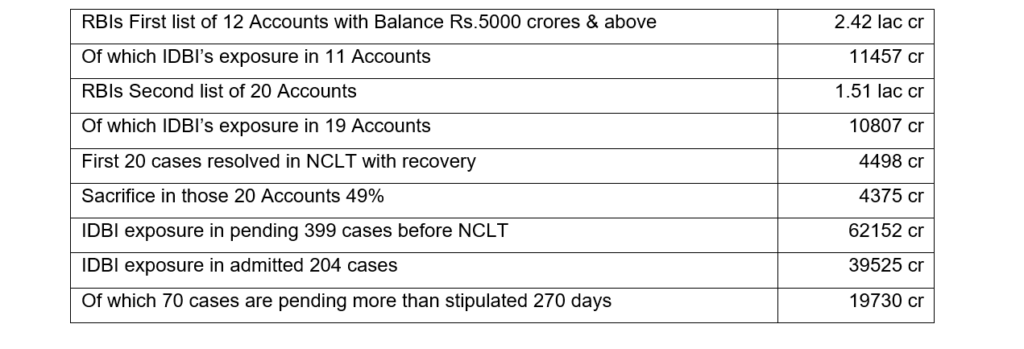

In 2017 government came out with Insolvency & Bankruptcy Act as a final solution to recover bad debts from big corporate and it was being claimed as a game changer by the government and also by the experts, academicians and industry representatives. Above data is self-explanatory. All this is about resolution process in which once the account is settled with whatever haircut, borrower gets clean chit and they can come out with new ventures and is free to raise fresh debt again from the financial institutions. Thus IBC has become enabling policy prescription for the corporate to wriggle out from debt by obtaining huge haircut. It is the bank which ultimately has to sacrifice. This is the reason why banks are incurring losses and thus the government is required to infuse capital by providing in the budget out of taxes collected from common man which money otherwise would have been spent on the welfare of needy people or in strengthening infrastructure to upgrade the lives of the common man. There are around 15 cases in which IDBI carried out liquidation proceedings against the corporate borrowers with an amount outstanding of Rs. 1122 crores in which after completing the process IDBI could recover Rs. 19.92 crores only. Of 204 cases of IDBI admitted in NCLT 70 cases are pending for a period more than 270 days which is the stipulated period in which all those proceedings should be over in which amount involved is Rs. 19,730 crores.

BANK PRIVATISATION: – SHOULD WE PERMIT BANK DEFAULTERS TO BECOME BANK OWNERS?

The above figures speak out that it is the corporate that too big corporate who has looted the hard earned savings of the common man and also has abused with the scarce resources with the government which were deployed to IDBI in the form of infusion of the capital. All the above affairs have resulted in deep crisis in IDBI Bank and now the government by using it as a justification is handing over IDBI again to the same corporate who has looted the bank. This government is doing it through a different route. Initially this bank has been handed over to LIC and in the days to come LIC will transfer its stake in IDBI in phases to private corporate. Thus the same corporate who has looted IDBI is day dreaming to be the owner of IDBI to subserve their own vested interests. This will jeopardize the interests of the common man just on the lines of PMC Bank in which case around 32 customers have lost their lives in last two years due to shock that they have lost their hard earned precious money. In case of Rupee Co-operative Bank from Pune the customers are on street since last 8 years but still they are unable to get their money back. In case of Karad Bank it was Bank of India which came to the rescue of the depositors while in case of Global Trust Bank it was Oriental Bank of Commerce who bailed out while in case of United Western Bank it was IDBI which saved the precious savings of the customers of United Western Bank. As we all are aware recently one of the new generation private sector bank “YES Bank” was about to collapse but it was State Bank of India who at the instance of the government bailed out ailing YES Bank. It was LIC & State Bank, public sector financial institutions, who bailed out systemically important and biggest Non Banking Financial Company “IL & FS” to avert systemic crisis in the financial world. Now, as is being said by the government official’s, government is likely to come out with one more financial institution to cater to long term finance or refinance to big infrastructure projects and if it is so then what was the propriety in converting IDBI into commercial bank and in turn in corporatizing IDBI and now in privatizing it? Is it not self-defeating? Is it not self-contradictory? Who is responsible for killing this pride institution IDBI?

AIBEA STANDS FOR PUBLIC SECTOR BANKING

AIBEA, pioneer union representing largest contingent of the bank employees, one which was instrumental in nationalization of the banks, stands for, to question the government, RBI and all those who are concerned with it. We demand for recovery of entire dues from all those big corporate and if they are recovered IDBI can generate required capital and government need not have to provide the capital to IDBI and thus the question of privatization does not arises at all. In order to recover those dues government should treat willful default as a CRIME and for that necessary amendments should be carried out in Indian Penal Code. AIBEA demands for publication of list of bank defaulters and they be prohibited from contesting elections by carrying out necessary amendments in election laws. AIBEA further demands for the accountability for sanctioning of the loans to fix up the responsibility on the authorities concerned and the guilty be punished for abusing public money. AIBEA also demands for stringent legal framework for effective recovery of bank dues more particularly from big corporate.

At a time when the economy of the country is witnessing unprecedented downturn with GDP recording negative growth for the first time in the last 24 years in the first quarter of 2020-2021 after declining for successive quarters for the last five years and the Government of India is harping on the imperativeness of implementing “Atma Nirbhar” policy to attain self reliance and RBI has also issued the discussion paper that moots the idea of long term finance bank, the contemplated move of Government of India to privatise IDBI Bank in its entirety is unfortunate and unwarranted. We fervently appeal to all the Hon’ble Members of Parliament, Members of Legislative Assembly and all people’s representatives to extend their support to us in saving IDBI Bank and hard earned saving of the customers of IDBI Bank by representing to the Government with a plea that the privatisation of IDBI is neither in the interest of the employees and officers of IDBI, nor in the interest of customers of IDBI nor in the interest of people at large or the economy. We the employees of IDBI resolve to do whatever is incumbent on our part to save IDBI being privatised and in our endeavour we appeal to all our esteemed customers, people’s representatives and people at large and all those who stand for the development of this nation to extend their support in our campaign.

“SAVE IDBI, SAVE ITS PUBLIC SECTOR CHARACTER”. Let us move together, Let us March together to defeat privatization of IDBI to protect our own savings, to protect interests of the nation.

Excellent article. Let us not demolish the Public Sector Character of any institutions and bring back Public Sector Character of IDBI.It is no doubt that lending by Public Sector Banks are mainly instrumental in Economic development in India from 1969 particularly in Agriculture. Retail and Small industries sector. Moto of PSU is profit with development wherein objective of Private Sector organizations is only profit. Please check the quality and quantity of lending by private sector banks to neglected sectors . Is it really lending to direct lending to Agrl. Retail or small and micro industries? The cat will be out of bag. Lending by Public Sector Bank is still the pivot of Indian economy. Let us not force them to die. IDBI once the piller of Industrial growth in India with excellent appraisal team should be brought back to it’s earlier public sector character. This is not duplicate at all.

Save idbi

Save Idbi

Should remain as public sector bank

Privatising IDBI Bank is not a solution. Better to Stop from NPA and strict measures to be taken against defaulterd by the Govt.

Character of IDBI Bank as a PSB is necessary for development of India.

Remain the character of IDBI BANK as a Public sector bank.

SAVE IDBI, SAVE ITS PUBLIC SECTOR CHARACTER

Government should provide the capital to the Idbi bank as same is majorly responsible for the NPAs. Further Idbi like institution is need of the hour for further growth of infrastructure.

I strongly support IDBI Bank to be maintained as Public sector Bank. Privatization is not the solution. Big Projects held up for long time for which IDBI Bank is not responsible.

Save and retain public sector character of IDBI Bank and also save other public sector too, do not sell it ro private holders