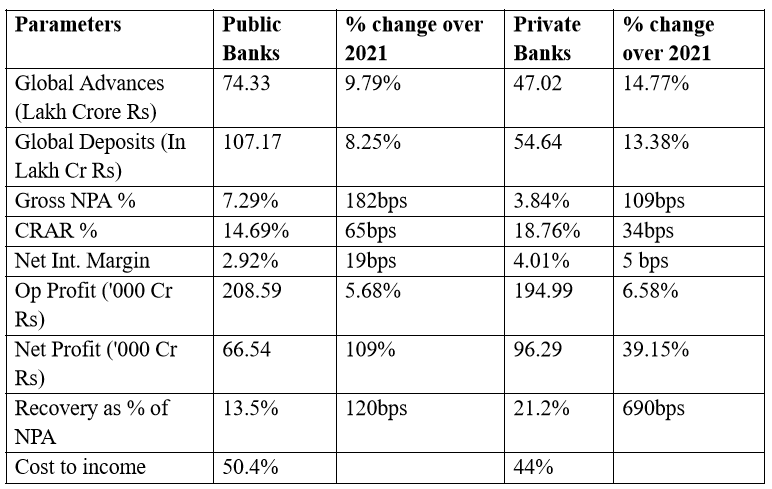

The net profit of the public sector banks in 2021 was Rs.31,820 crore and their operating profit was Rs.1,97,376 crore. The net profit increased by 109% to Rs.66,541 crore in 2022 and the operating profit increased to Rs.2,08,591 crore.

Though the performance of public sector banks should not be compared to private sector banks, the government of India continues to pitch them against each other. Private banks are for profit generation for their shareholders. Whereas public sector banks give services to the people, make credit reach the last mile and fulfil government objectives through schemes like the Jan Dhan Yojana, Mudra Loans, PM Svanidihi, Atal Pension Yojana etc.

The performance of public sector banks should be assessed based on the constitutional goals of a welfare state; to bring down inequality, provide equal opportunities to all and provide job reservations.

In an annual review conducted by the Finance Ministry, a report was presented on 20.06.2022 in 37 slides. As per the parameters, this is the performance of public sector banks and private sector banks in 2021-22.

If we analyse the performance of public sector banks vs the private sector banks (Top 5) in no way public sector banks are faring poorer. In many parameters they are similar, and in a few, they are better. The CD Ratio has to improve.

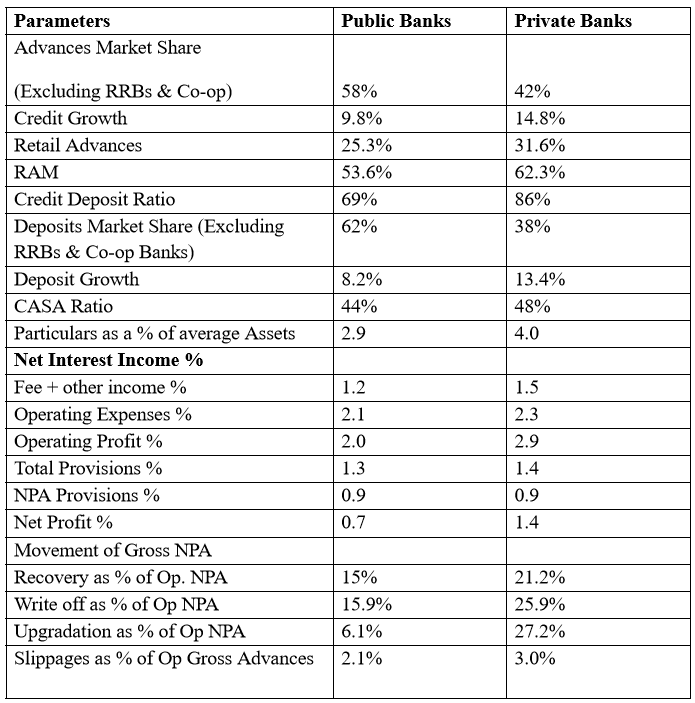

Let us look at some more data which is not taken up for comparison in the report.

If we look at the segment-wise growth in advances of public sector banks, it is 34.5% compared to the corporate sector. There is a growth of 10.5% in agriculture advances, 10.5% growth in MSME advances and 18.8% growth in retail advances. This is going to be dangerous in the future.

Gross NPAs of PSBs in the corporate sector are Rs.2,50,739 cr, while in the MSME they stand at Rs.1,30,987 cr, in agriculture the same is Rs.1,25,066 cr and in retail, it is Rs.35,381 cr.

So it is clear that corporate advances are a grey area. Gross NPAs in advances above Rs.100 crores from 1085 accounts are Rs.1.64 lakh crores. The Finance Minister has reviewed these accounts, but we don’t know what action she has taken. If they are going to be referred to NCLT the banks will lose almost everything and the corporates will benefit. Frauds are reported in exposures above Rs.100 crores in 80 accounts of public banks and 38 accounts of private banks. The amount is Rs.28,800 cr for public banks and Rs.13,000 cr for private banks. These are not likely to come back.

The public sector banks could raise Rs.40,368 cr as bond capital and Rs.10,351 cr as equity capital. The market capitalisation of public banks is shown as 6,63,203 cr and of the top 5 private banks as Rs.18,27,975 cr which is not at all the true value of these banks. Everyone knows the gamble in the stock market.

Look at HDFC Bank, the top among the private banks. They have 6,342 branches of which only 1,147 (18%) are rural, 2,036 (32%) are semi-urban, 1,312 (21%) are urban and 1843 (29%) are metro. They have 7.1 crore customers. So the number of customers per employee is just 501. They have a staff strength of 1,41,579 employees. Their total business is Rs.29,28,037cr (Dep 15,59,217 + Advances 13,68,820).

Now let’s look at the State Bank of India. SBI has 46.77 crore customers, 6.58 times more than HDFC Bank. It has a business of Rs. 67,85,501 cr which is 2.31 times of HDFC Bank. Its staff strength is 2,44,250, 0.5 times more than HDFC. Interestingly, while HDFC recruited 21,486 staff last year SBI reduced its staff by 1402!

BOB has a total business of 18,23,093 cr, with 8,168 branches of which 34.82% are rural, 25.5% are semi-urban, 18.06 urban and 21.62% metro. BOB has more than 13 crore customers and only, 79,000 employees, which is just half of HDFC’s staff strength.

If staff strength is increased in the public sector, their business, customer service and profits will certainly improve. PSBs also provide reservations, including a 7.5% reservation to economically weaker sections among the forward caste. Their annual reports provide all details about it, but none of that happens in reports of private banks.

Instead of helping public sector banks, the government is talking of privatising them. Newspapers are reporting that the Banking Laws Amendment Bill is soon expected in the monsoon session of the Parliament.

This will completely deprive the unorganised sector of access to credit. 90% of the population will have to depend on Non-Banking Finance Companies (NBFCs), Micro Finance Institutions (MFIs) and the unreliable loan apps which are killing people.

Recently Dr. Sailendra Babu, DGP Tamil Nadu has appealed to the public not to use these loan apps which are using abusive methods of recovery. A person in Chennai has committed suicide after taking a 5000 rupees loan, from which only Rs. 3600 were actually credited to his account. On top of that, to recover the money, the agents employed by the loan app, got hold of his photos, morphed them and circulated them among his family and friends.

Should this be the fate of our people? Suicides due to MFIs and NBFCs are becoming very common. Even the much appreciated Mr. Siddharth of Coffee Day committed suicide due to these kinds of loans.

The unions and associations have to be aware. There is a well-planned effort to encourage unions and associations that support the government or take over the leadership of unions and associations by infiltrating them or by splitting them, saying unions and associations should be apolitical.

Unless the unions and associations go to the people, and the customers and explain the facts and mobilise massive actions, the future of the banking sector is in peril. Loan sharks will have a field day in the absence of corrective action.

Thomas Franco is the former General Secretary of All India Bank Officers’ Confederation and a Steering Committee Member at the Global Labour University.

Centre for Financial Accountability is now on Telegram. Click here to join our Telegram channel and stay tuned to the latest updates and insights on the economy and finance.

Wonderful message from Mr.Franco sir.

Further, as per their Govt review itself, the performance of PSBs in Mar2022 under the vital parameters (write-off& Slippages) is much better than Private Banks (Page 23/37). Why can’t the Govt. nationalize a few top private banks in the interest of national growth?

I hope the Govt will keep their issue pending for another 6-8 months and have a new look on.